The USDT PSM was launched with a seed allocation of 216k USDT. Initially the fees were set at 1% then reduced at 0.1%. A PSM front end was also launchedThe protocol earned 1.2k VAI in the process (not that it is the goal of the PSM).

Nonetheless, the PSM is now depleted and the Venus community should decide how to move forward in the quest of getting VAI pegged again. The treasury is ~6M as we speak with only 1.3M USDT.

There are two solutions:

- Deposit more USDT in the PSM

- Increase the VAI borrow rate either through the

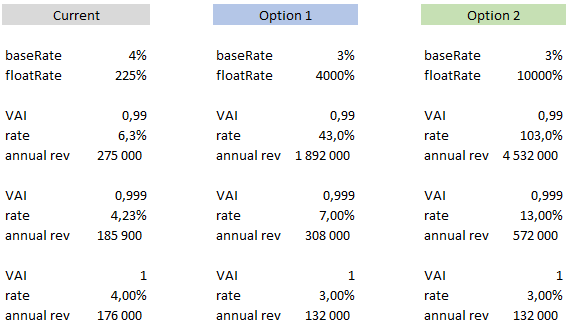

baseFeeor thefloatFee

Ideally depositing 4.2M USDT to the PSM would solve the problem as there is only 4.2M VAI outstanding that can be redeemed. Sadly the Venus Treasury doesn’t have that much and it is also used to fund expenses.

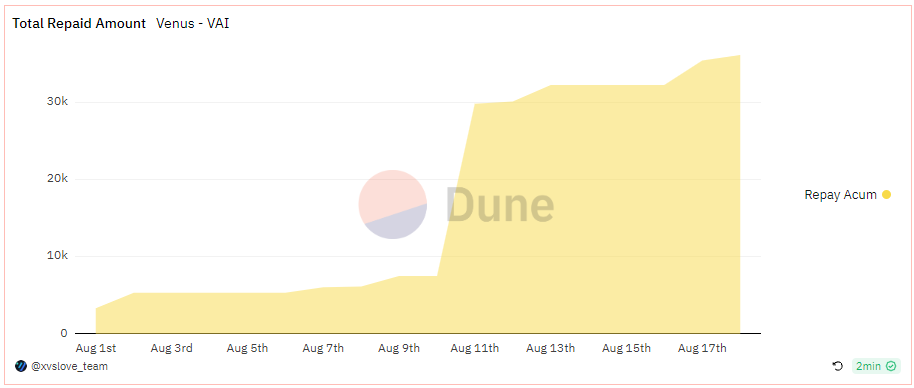

The protocol is currently earning 6% on the VAI loans (around 4.4M outstanding), around 275k VAI per year. The increase of the baseRate didn’t had much impact on VAI borrowers as you can see in the graph below showing the cumulative repayment since August 1st. It’s only 32k VAI (most of which was before the PSM).

Part of the borrowers are borrowing VAI against USDT which means they are bleeding money right now (interest received on USDT is below interest paid on VAI) and are maybe expecting a bigger depeg of VAI (or just not monitoring the situation).

One solution is to penalize the borrowers that are still borrowing when the PSM is empty by significantly increasing the floatRate (see two options below). As a tradeoff, we suggest lowering the baseRate.

The high level strategy would be the following:

- When VAI = 1 USDT (PSM would start to accumulate USDT) then VAI borrow rate would be the cheapest on Venus, incentivizing people to borrow in VAI instead of other stablecoins.

- When VAI = 0.999 USDT (meaning the PSM gets depleted of USDT) the VAI borrow rate would be the most expensive on Venus against other stablecoins incentivizing people to refinance in USDT or USDC

- When VAI < 0.999 USDT (the PSM is depleted) there would be significant increase in VAI borrow rates leading at some point to liquidations.

As discussed above, VAI borrowers should refinance with USDT as it is cheaper.

It is also good to note that the VAI vault currently provides a 7.88% APY in XVS. We haven’t evidence that this arbitrage is significant, but some borrowers could use it and could therefore still be happy to pay 6.3% to earn 7.88%.

We therefore ask for Venus community inputs so we can provide a proposal that match your wishes.