Proposal: Market Risk Management

Summary

A proposal for continuous market risk management to optimize yield, capital efficiency, and mitigate depositor losses.

Background

Venus’s previous interest rate model and conversations with the Venus team shows the importance protocol stakeholders put towards understanding and mitigating risk. Over the past few years, Gauntlet has deployed our simulation platform to similar lending protocols and we are happy to state Gauntlet’s work has resulted in strengthening protocol structure and we continue to make parameter recommendations to optimize for capital efficiency as well as reduce insolvency risk.

Preventing insolvency is not the only market risk Venus faces. Deflationary spirals and shocks to market prices can’t simply be prevented without reducing the protocol’s utility. Tail-event scenarios are rarely the result of bad actors taking malicious actions against the protocol. The vast majority of Venus’s participants are honest but what’s good for the lender is not always good for the borrower. Depositors lend, borrowers borrow, and liquidators rebalance. This intersection is where Gauntlet comfortably sits, directing traffic per the stated desires of the community.

Gauntlet will onboard and then continuously rerun our simulations for the Venus Protocol, pushing regular changes to ensure optimal risk parameters. We will also deploy our asset listing framework to ensure new assets being proposed for the Venus Protocol meet the market risk standards that the community has set forth.

Proposal

The initial proposed scope will control for the target metrics Gauntlet aims to improve. Those metrics are:

- Value at Risk

- Liquidations at Risk

- Borrow Usage

Gauntlet will improve the metrics above without increasing the net insolvent value percentage or the slashing run percentage.

Expectations

- Risk Parameter Updates

- Exclusively for Venus Protocol assets

- Isolated pools with a 30-day average supply >$5M USD

- Supported Risk Parameters: Loan-To-Value, Liquidation Threshold, and Liquidation Bonus

- Market conditions will determine the frequency of updates. For that reason, no SLA will be preset.

- Exclusively for Venus Protocol assets

- Communications

- Risk parameter changes will follow the standards suggested from the Venus core team.

- Risk Dashboard (refer to the next section)

- Quarterly Risk Reviews will provide a detailed retrospective on market risk.

- Out of Scope

- Modeling and support for the VAI stablecoin.

- Protocol development work (e.g. smart contract upgrades that improve risk/reward).

- Formalized mechanism design outside of supported parameters.

- Oracle and smart contract risk analysis (e.g. smart contract or oracle audits).

- Developing strategies to resolve existing bad debt.

- Dashboard and long form written analysis for isolated pools.

Risk Dashboard

As part of this engagement, Gauntlet will build a Risk Dashboard for the community to provide key insights into risk and capital efficiency.

The dashboard focuses on the system-level risk in Venus and the market risk on an individual collateral level. Our goal is to help convey Gauntlet’s methodology to the community and provide visibility into why Gauntlet is making specific parameter recommendations.

The dashboard will monitor all collateral assets in Venus. The three key metrics are Value at Risk (VaR), Liquidations at Risk (LaR) and Borrow Usage.

Value at Risk conveys capital at risk due to insolvencies when markets are under duress (i.e., Black Thursday). The current VaR in the system breaks down by collateral type. Gauntlet computes VaR (based on a measure of protocol insolvency) at the 95th percentile of our simulation runs.

Liquidations at Risk conveys capital at risk due to liquidations when markets are under duress (i.e., Black Thursday). The current LaR in the system breaks down by collateral type. Gauntlet computes LaR (based on a measure of protocol insolvency) at the 95th percentile of our simulation runs.

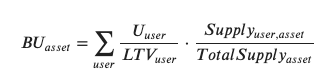

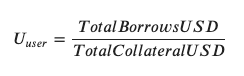

Borrow Usage provides information about how aggressively depositors of collateral borrow against their supply. Defined on a per Asset level as:

where U is the utilization ratio of each user:

Gauntlet aggregates this to a system-level by taking a weighted sum of all the assets used as collateral.

To show Gauntlet’s impact, we measure these using the current system parameters and expected results (based on our simulations) if Venus implemented the proposed parameter recommendations.

Structure

Gauntlet charges a service fee that seeks to be commensurate with the value we add to protocols. We are offering Venus a 20% discount for a 2 year engagement bringing the contract value to $1.6M USD: this includes support for up to 50 assets on the core protocol, and coverage for isolated pools with a 30-day average total supply of >$5M. Gauntlet also wants to provide a strong signal of our alignment with the protocol. For that reason, we propose a fully refundable (up to 4 weeks prior to start date) deposit in stablecoin, and our contractual fee denominated in either stablecoin or $XVS. In addition, Gauntlet will deploy either the Sablier or Llama Pay contract for the 2 year engagement to provide the community a revocable option should our impact or engagement be deemed unsatisfactory.

About Gauntlet

Gauntlet is a simulation platform for on-chain risk management. Gauntlet uses battle-tested techniques from the algorithmic trading industry to help protocols manage risk, fees, capital efficiency, and incentives. Our agent-based simulation models optimize parameter decisions for tens of billions of dollars in DeFi TVL. Our prior work, includes assessments or continuous financial modeling for Compound, MakerDAO, Aave, Liquity, and many others.