Summary

We recommend reducing collateral factors (CF) across three asset groups in the Venus BNB Core Pool: volatile assets, LSTs, and stablecoins.

Context. Several Core Pool assets are less liquid or more volatile than current CFs support. Liquidation thresholds will remain unchanged, so no existing position is liquidated due to this change.

Recommendations

| Asset | Group | CF: Current → Rec | Note |

|---|---|---|---|

| asBNB | LST recalibration | 72% → 60% | Low liquidity |

| slisBNB | LST recalibration | 80% → 72% | Reducing to sub-BNB CF |

| wBETH | LST recalibration | 80% → 60% | Low liquidity |

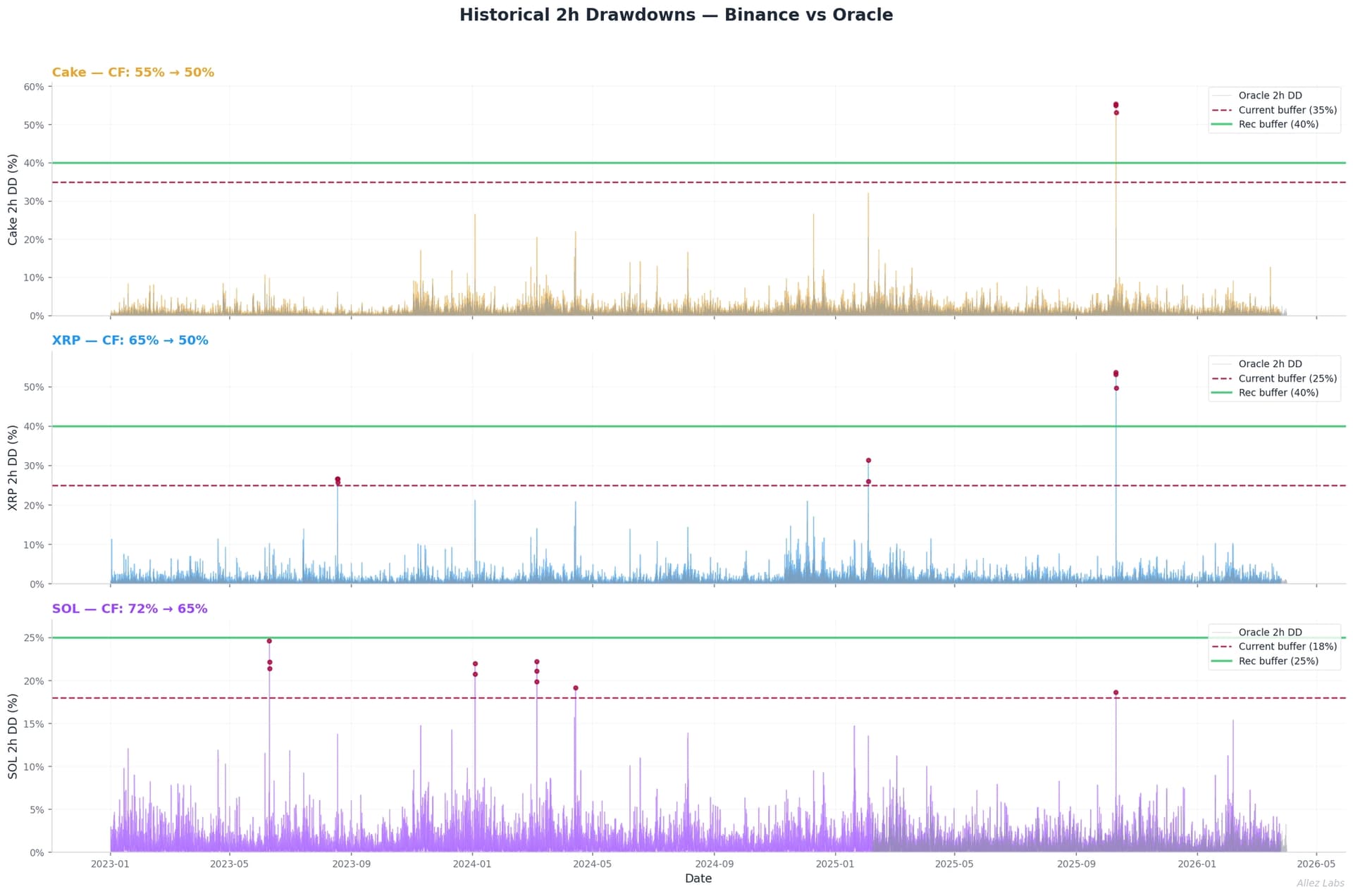

| XRP | Volatile Asset | 65% → 50% | Calibrated to EVT 5yr 2h |

| SOL | Volatile Asset | 72% → 65% | Calibrated to EVT 5yr 2h + liquidity on chain |

| USDe | Stable | 75% → 50% | Minimal BSC DEX depth |

| FDUSD | Stable | 75% → 50% | Minimal BSC DEX depth |

| PT-sUSDE | Stable | 70% → 0% | Expired token (matured Jun 2025) |

Volatile Assets

CF has been sized to appropriately capture increased volatility and tightened liquidity of several tokens across several metrics including the 2h-window EVT drawdown estimate (CF set to the 5yr 2h return level).

EVT 5-Year Return Levels (2h Window)

| Asset | Current CF | Rec CF | Buffer | EVT 5yr 2h | Margin | Oracle 2h Max |

|---|---|---|---|---|---|---|

| XRP | 65% | 50% | 40% | 39.5% | +0.5pp | 18.6% |

| SOL | 72% | 65% | 25% | 25.8% | -0.8pp | 9.4% |

Buffer = 100% − recommended CF − 10% liquidation incentive: the price drop a max-leveraged position absorbs before liquidation proceeds no longer cover debt plus bonus.

LST Recalibrations

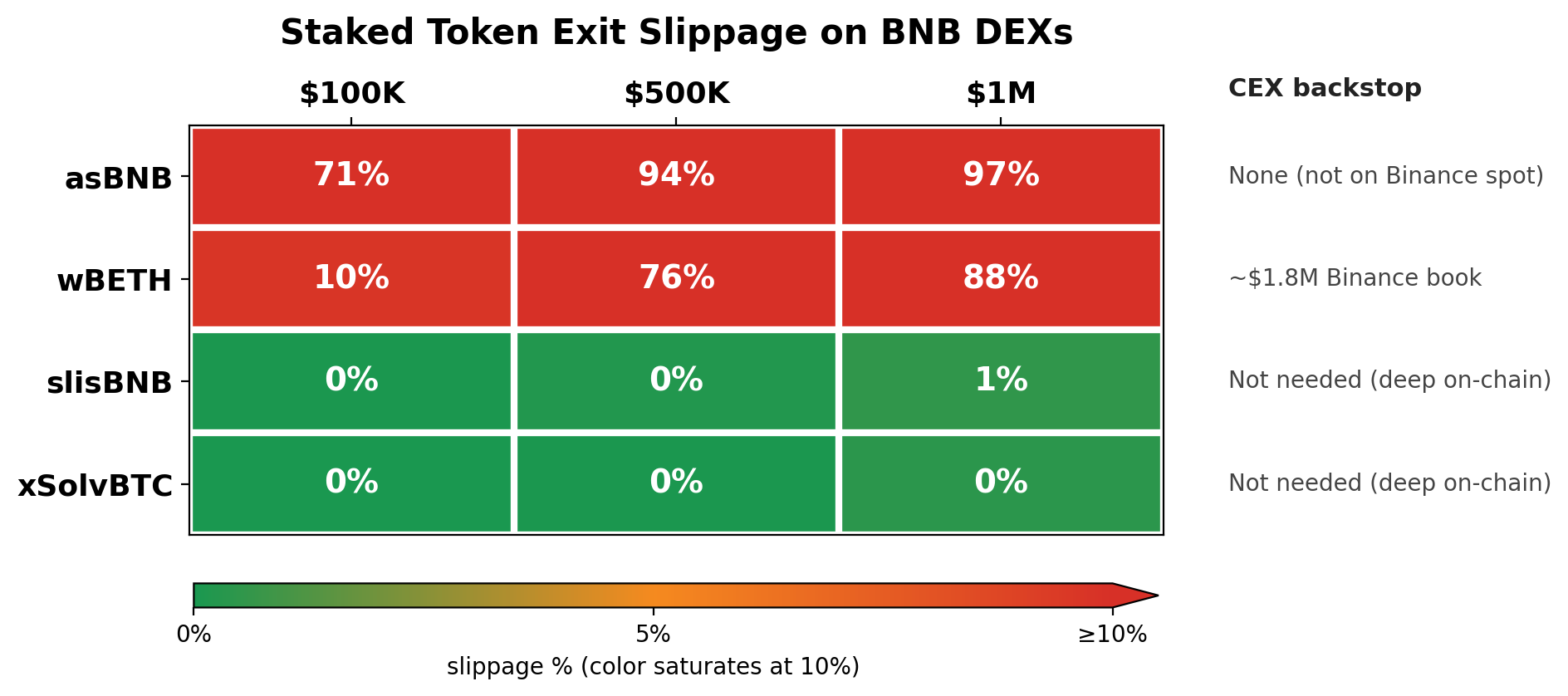

Each LST below inherits its underlying’s market risk plus issuer, slashing, and redemption-delay risk, and trades with thinner DEX liquidity than the underlying. An LST’s CF must therefore sit strictly below its underlying’s. At present, slisBNB and wBETH both sit at 80%, tied with BNB and ETH respectively.

Each of these assets has a very different liquidity profile, with some issuers supporting deep liquidity on chain. Slippage selling each LST into USDT across BSC DEXes, PMMs, and limit-order books:

asBNB has about $30K of DEX liquidity against $87M of supply while wBETH has about $122K on-chain plus a ~$1.8M Binance backstop against $23M. Native redemption is too slow to backstop liquidations, as asBNB redeems to slisBNB only over a 3 to 5 day window depending on launchpool state. Other LST issuer redemptions (7 to 15 days) are similarly too slow to keep pace with price-driven liquidations. slisBNB and xSolvBTC liquidity are materially more robust than comparative derivative tokens.

First-round liquidations triggered under a basket-aware shock, where BNB, ETH, and BTC family debt moves with the correlated collateral:

| Asset | -10% | -20% | -30% |

|---|---|---|---|

| asBNB | $0 / 0 wallets | $251K / 11 | $620K / 28 |

| wBETH | $4.48M / 6 | $4.52M / 15 | $4.54M / 23 |

| slisBNB | $0 / 0 | $0 / 0 | $1.1K / 2 |

| xSolvBTC | $1.8K / 1 | $2.7K / 2 | $4.6K / 4 |

wBETH has weak DEX liquidity: a 10% price drop may force $4.5M of liquidations into a market that absorbs ~$122K (not accounting for Binance markets) before material slippage while asBNB has room for about $600K of single sided sell pressure before such slippage.

| Asset | Liquidity | Current CF | Rec CF | Rationale |

|---|---|---|---|---|

| asBNB | Thin | 72% | 60% | $30K exit vs $87M supply; halt new stablecoin borrows |

| wBETH | Thin | 80% | 60% | $4.5M liquidation pressure at -10%; also fixes the ETH tie |

| slisBNB | Deep | 80% | 72% | Recalibrate below BNB; deep liquidity supports borrows |

| xSolvBTC | Deep | 72% | 72% | Deep on-chain; >99% of collateral use already in BTC eMode |

The lower 60% CF on asBNB and wBETH will stop new high-leverage stablecoin borrowing, without forcing existing users out. slisBNB and xSolvBTC are deep enough to support liquidations, so they move to / remain at an enhanced LST CF.

Stablecoins

While stablecoins are the dominant borrow asset class on Venus BNB (>$179M in outstanding borrows), the protocol also has material exposure to stables as collateral. We recommend reducing the borrow power of several less liquid stablecoins to a CF of 50% (FDUSD and USDe) while removing collateral eligibility for the expired PT-sUSDE.

Despite the CF changes, all Venus use-cases are preserved. Depositors for impacted stablecoins will continue to earn supply yield, while users wishing to borrow against stable assets can do so via a smaller collection of stables, which carry deep DEX liquidity to support liquidations at scale. The change redirects collateral use toward assets the protocol can safely liquidate, while continuing support for a broad range of stables as borrowable assets. The below tables show the DEX liquidity across stablecoins.

DEX liquidity across stables (price impact at trade size):

| Token | $100K | $500K | $1M | $2.5M | $5M | Max size <1% |

|---|---|---|---|---|---|---|

| USDC | <0.05% | <0.05% | <0.05% | <0.05% | <0.05% | >$5M |

| USDT | <0.05% | <0.05% | <0.05% | <0.05% | <0.05% | >$5M |

| U | <0.05% | <0.05% | <0.05% | <0.05% | 1.00% | >$5M |

| FDUSD | <0.05% | 65.52% | 82.41% | 93.59% | 96.78% | $100K |

| USDe | 70.21% | 94.04% | 97.01% | 98.80% | 99.40% | <$100K |

| USD1 | <0.05% | <0.05% | 0.10% | 1.10% | - | ~$1M |

| lisUSD | <0.05% | <0.05% | <0.05% | 0.18% | - | ~$2.5M |

Recommended CFs:

| Token | CF: Current → Rec | Debt Impacted | Rationale |

|---|---|---|---|

| USDe | 75% → 50% | $11K | Thin DEX depth; 70% price impact at $100K |

| FDUSD | 75% → 50% | $5M | DEX depth exhausted above ~$100K |

| PT-sUSDE | 70% → 0% | ~$0 | Expired token, matured June 2025 |

Allez Labs has not been compensated by any third party for publishing this recommendation.