[VRC] Venus Dual-Vendor OEV Trial: Chainlink SVR Performance Report

Hi everyone, this is Esteban Garcia from Chainlink Labs. I’d like to share a performance report on Venus Protocol’s use of both Chainlink Smart Value Recapture (SVR) and RedStone for recapturing oracle-related, non-toxic liquidation MEV (i.e., OEV).**

Over the trial period, two OEV recapture solutions were run side by side on BNB Chain to judge their security, reliability, and recapture performance. In the entire period, Chainlink SVR materially outperformed RedStone on the two metrics we believe are most important for Venus DAO to evaluate:

(1) Revenue generation per dollar of available liquidation value, and

(2) Decentralization of active liquidator participation as a proxy for security of OEV solutions

Summary of performance:

| Chainlink SVR | RedStone | |

|---|---|---|

| Total OEV Recaptured | 128.08 BNB | 28.15 BNB |

| Revenue Generation (percent recaptured of available) | 29.04% | 2.23% |

| Decentralization (# of Active Liquidators Observed) | 8 | 1 |

These results matter not only for DAO revenue, but also for protocol resilience. A more competitive and broader liquidator ecosystem improves both value capture and operational robustness during volatile market conditions. Based on the observed trial results, we observe Chainlink SVR has proven itself to be the strongest solution on the metrics most relevant to Venus DAO.

Background

Since going live, Chainlink SVR has recaptured 128.08 BNB in OEV for the Venus DAO while introducing zero bad debt. Venus has gained a new, recurring revenue stream built on top of the same battle-tested Chainlink infrastructure that has secured the protocol since 2020. This track record speaks to what SVR was built for: performing reliably when markets are at their most volatile.

For broader context, across all Chainlink SVR deployments (Aave, Compound, Morpho and Venus), SVR has reliably processed over $700M+ in user liquidations and recaptured over $18.6M in OEV, including during the most extreme market conditions; such as the October 10, 2025 volatility event, which triggered the largest liquidation cascade in crypto history. SVR maintained full operational integrity throughout, continuing to deliver timely price updates and facilitating orderly liquidations.

Chainlink SVR, which is underpinned by the same decentralized oracle network (DON) infrastructure that powers over 65% of DeFi by Total Value Secured and has enabled over $30 trillion in transaction value, has continued to perform reliably throughout every period of heightened volatility since the Venus integration, including major market-wide sell-offs. Price feeds have maintained consistent, timely updates. This reflects over half a decade of production hardening and decentralized architecture, where security and uptime remain our first priority.

We appreciate the Venus community’s trust and partnership. The relationship between Chainlink and Venus dates back to 2020, and we view SVR as the next chapter in a collaboration that has delivered reliable oracle infrastructure through every market cycle. We’re excited to keep building on that foundation together. We encourage the Venus community to pick the more revenue generating and decentralized system to continue to power all of the Venus markets.

The numbers used through this post were gathered on the 4th of May.

Overview

Performance Metrics

We recommend the Venus DAO focus on two simple metrics for this decision:

1. The revenue each OEV system generates.

This is measured as a % of the revenue that was possible to generate from the liquidations. It answers the question: “if $100 of liquidation bonuses were triggered by oracles on Venus, how much of that was recaptured by the system”? This metric is the current industry standard for evaluating OEV performance used by all integrated protocols and their communities. We believe this is the clearest single metric for evaluating revenue-generation performance because it measures how much of the available liquidation value was actually returned to the DAO.

The performance as of the 4th of May is as follows for both systems:

Chainlink SVR: 29.04% of potential revenue was returned to the DAO.

RedStone: 2.23% of potential revenue was returned to the DAO.

2. The decentralization of each OEV system.

Measured in terms of the # of unique entities that have performed liquidations under that OEV system. This metric is incredibly important because it informs lenders on the platform of the safety of their assets, and there have been previous incidents of bad debt on Venus due to a lack of liquidators. Not having enough liquidators can leave the protocol with bad debt if nobody is clearing the system when it matters. The risk of further bad debt incidents like this may increase dramatically if a centralized OEV system is chosen.

The performance as of the 4th of May is as follows for both systems:

Chainlink SVR: 8 liquidators are securing the Venus protocol by performing liquidations.

RedStone: 1 liquidator is securing the Venus protocol by performing liquidations.

In summary, Chainlink SVR returned 29.04% of available liquidation value versus 2.23% for RedStone, and supported 8 active liquidating entities versus 1 for RedStone during the observed period.

Future Looking

SVR currently services all of the largest markets for stablecoin denominated loans against major assets in DeFi (BTC, ETH). Chainlink SVR can provide Venus with access to the same liquidator set currently servicing these markets across all major protocols and a majority of total DeFi TVL. It is our view that Venus choosing more centralized liquidator systems than Chainlink SVR would lower the risk-adjusted returns for Venus lenders, and discourage more professional capital from entering the Venus ecosystem.

Not only does Chainlink SVR capture more value to generate more revenue for the Venus protocol, it does so while having a more decentralized liquidator set. Highlighting the value of tapping into the network effects of the largest group of lending liquidators in DeFi.

OEV Analysis Framework

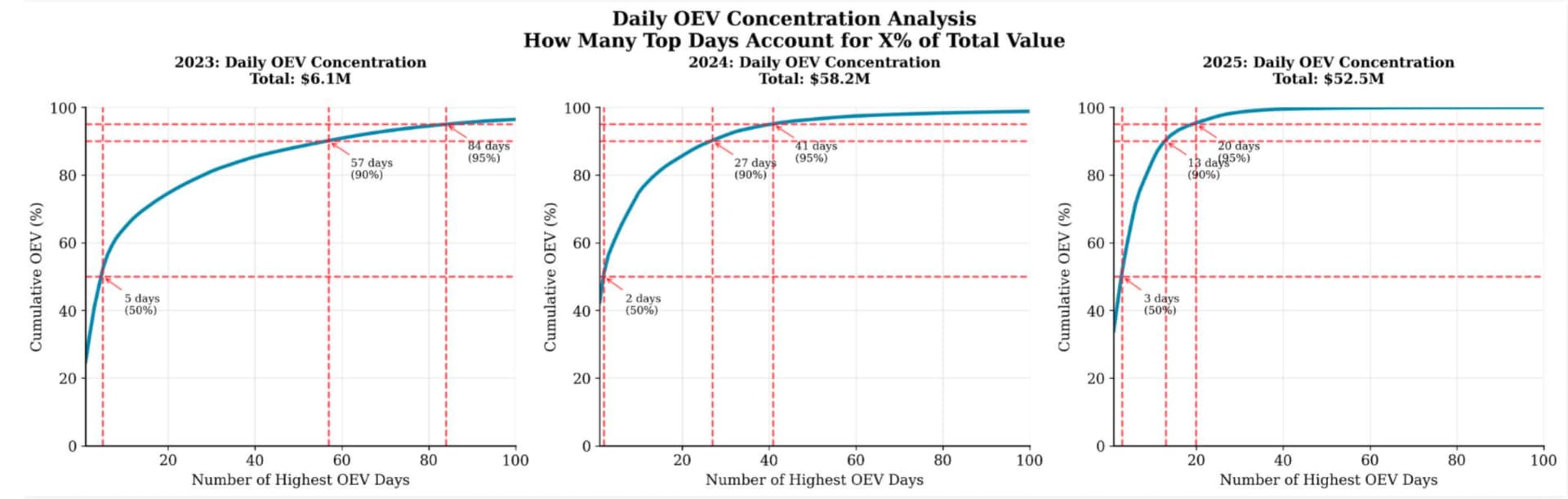

OEV systems need to perform during periods of market stress

The charts below show the percentage of OEV generated on Aave during different days in the year.

-

Just 2 days produced 50% of all liquidation value on Aave in 2024

-

Just 3 days produced 50% of all liquidation value on Aave in 2025

-

The top 1% of liquidation events = 54% of total OEV

[image]

What this shows is that OEV value is concentrated to a very small number of days per year. For that reason, Venus should prioritize systems that continue to function reliably during stressed market conditions. Failing to liquidate during the most volatile periods not only means you lose out on 50%+ of your revenue, it also exposes you to bad debt risk when markets need to get cleared.

Bottom line: OEV mechanisms must work during extreme market volatility, extreme events are not an excuse for poor performance, they are when your protocol should shine.

OEV systems must be permissionless and decentralized

DeFi protocols, including Venus itself have suffered in the past from bad debt due to an insufficiently sized liquidator network. The more decentralized and professional a liquidator network is, the greater safety for lenders on the protocol. All other major SVR integrations in production have relied on a permissionless auction with many participants; this is critical to the success of these protocols, and we feel it will also be critical to the success of Venus going forward. On Aave V3, more than 100 unique searches have been observed liquidating positions through Chainlink SVR.

A centralized single liquidator system alienates the existing community of Venus liquidators, and that community should not be expected to stick around and run their costly infrastructure if they cannot integrate to that OEV system. From a conservative risk management perspective, the DAO should assume that only 1 liquidator may exist on Venus markets secured by RedStone, and 8 liquidators exist on Venus markets secured by Chainlink SVR.

We would encourage the DAO to make its decision based purely on the products that were operated during the trial period. While RedStone may eventually implement an OEV auction with more than 1 bidder, this would be an entirely different product altogether from what RedStone operated during this trial period. Based on our 18-month experience operating OEV auctions, we understand that there are significant challenges in transitioning to a true auction, and that encountering these challenges in production as the sole OEV provider for Venus would introduce significant risk to Venus.

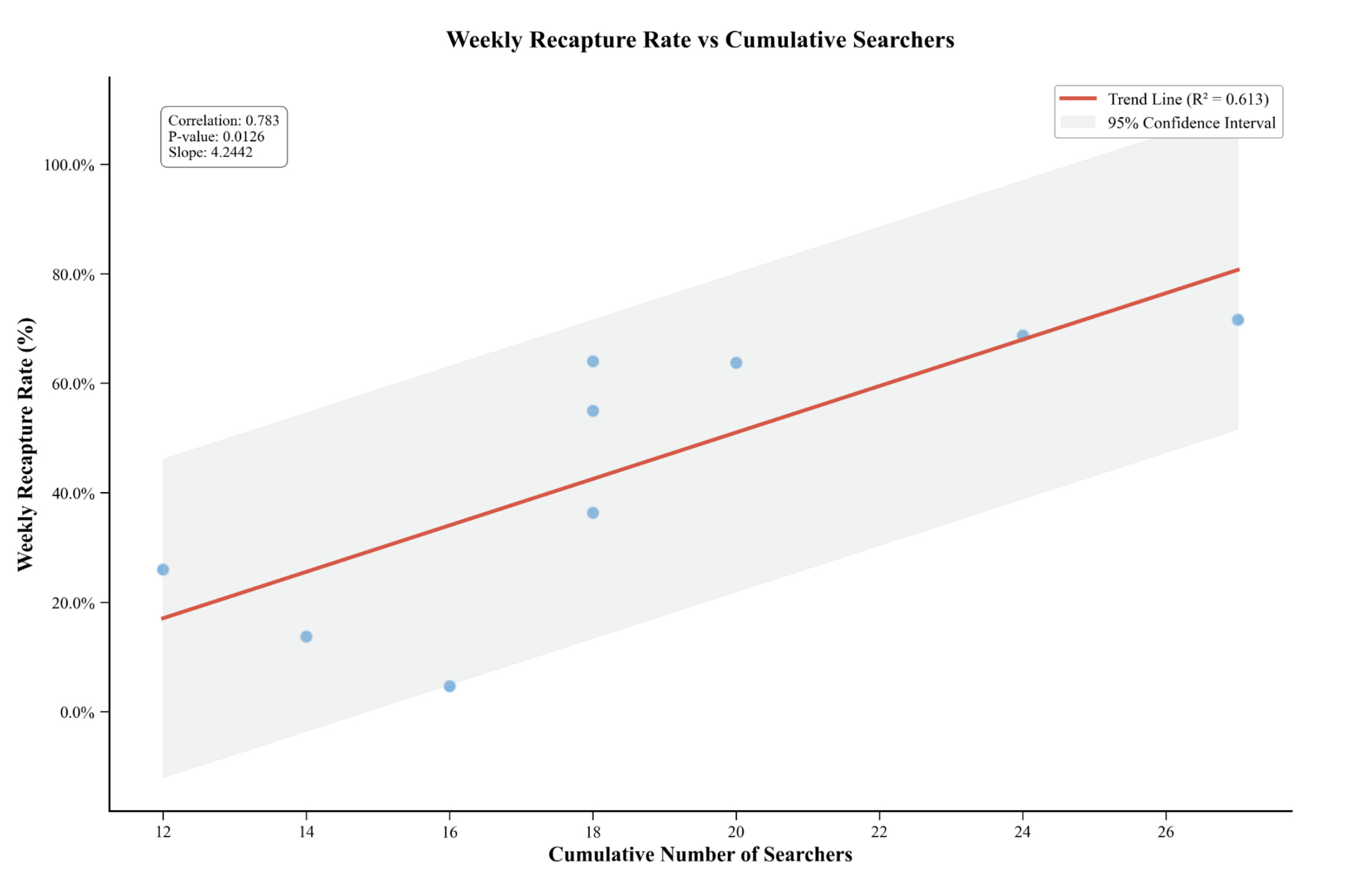

OEV systems generate more revenue as the liquidator set grows

Not only does a large liquidator set help secure the Venus protocol, but it also will lead to higher revenue. Here is some data from our time running SVR on other protocols that further illustrates the power of a permissionless auction with many liquidators:

[image]

As Chainlink SVR is a fully open and permissionless system, it is easy for liquidators to onboard. As more liquidators onboard our recapture rate has steadily increased due to the increased competition between the participants. This leads to higher revenue and less risk at critical times, Venus becomes more antifragile.

Quantitative Comparison of Performance

The analysis starts at the beginning of the trial period on February 4th, and runs until May 4th, 2026.

Revenue Generation Per Dollar Available Comparison

This metric is very simple, it tells you how well a system generated revenue based on the potential revenue available to the system. We take the total revenue generated by the OEV system, and we divide it by the total value of all liquidation bonuses that were triggered by the underlying data feeds from the OEV service provider. To illustrate this metric, imagine a price update creates two liquidation opportunities on Venus:

- Position A has $100 of available liquidation value

- Position B has $1,000 of available liquidation value

Suppose the OEV provider successfully captures the full $100 from Position A, but fails to capture anything from Position B.

Looking only at the liquidation it won, someone might say the provider achieved a 100% recapture rate on that event. But that would be misleading, because the provider captured only $100 out of $1,100 of total available value. Under the methodology used here, the provider’s performance would be measured as:

$100 captured / $1,100 available = 9.1% revenue generation per dollar available

This is why we believe this metric is the most useful for Venus DAO: it measures how much value was actually returned to the protocol relative to the total value that was available to be captured. Using the above methodology we arrive at the following metrics which show Chainlink SVR to be an order of magnitude ahead.

| Metric | Value |

|---|---|

| Recapture rate (Chainlink SVR) | 29.04% |

| Recapture rate (Redstone) | 2.23% |

Decentralization and security of the OEV system

To measure the decentralization and security, we analyzed the data to determine how many unique entities participated in liquidations for a given OEV system. In this method, we don’t look at just the number of unique contracts that won a bid, but we also look at who deployed these contracts. Using this method we found that Chainlink SVR on Venus has had at-least 8 unique liquidators active, while Redstone only has had 1 single active liquidator throughout the entire trial period.

| Metric | Value |

|---|---|

| Unique Liquidators (Chainlink SVR) | 8 |

| Unique Liquidators (Redstone) | 1 |

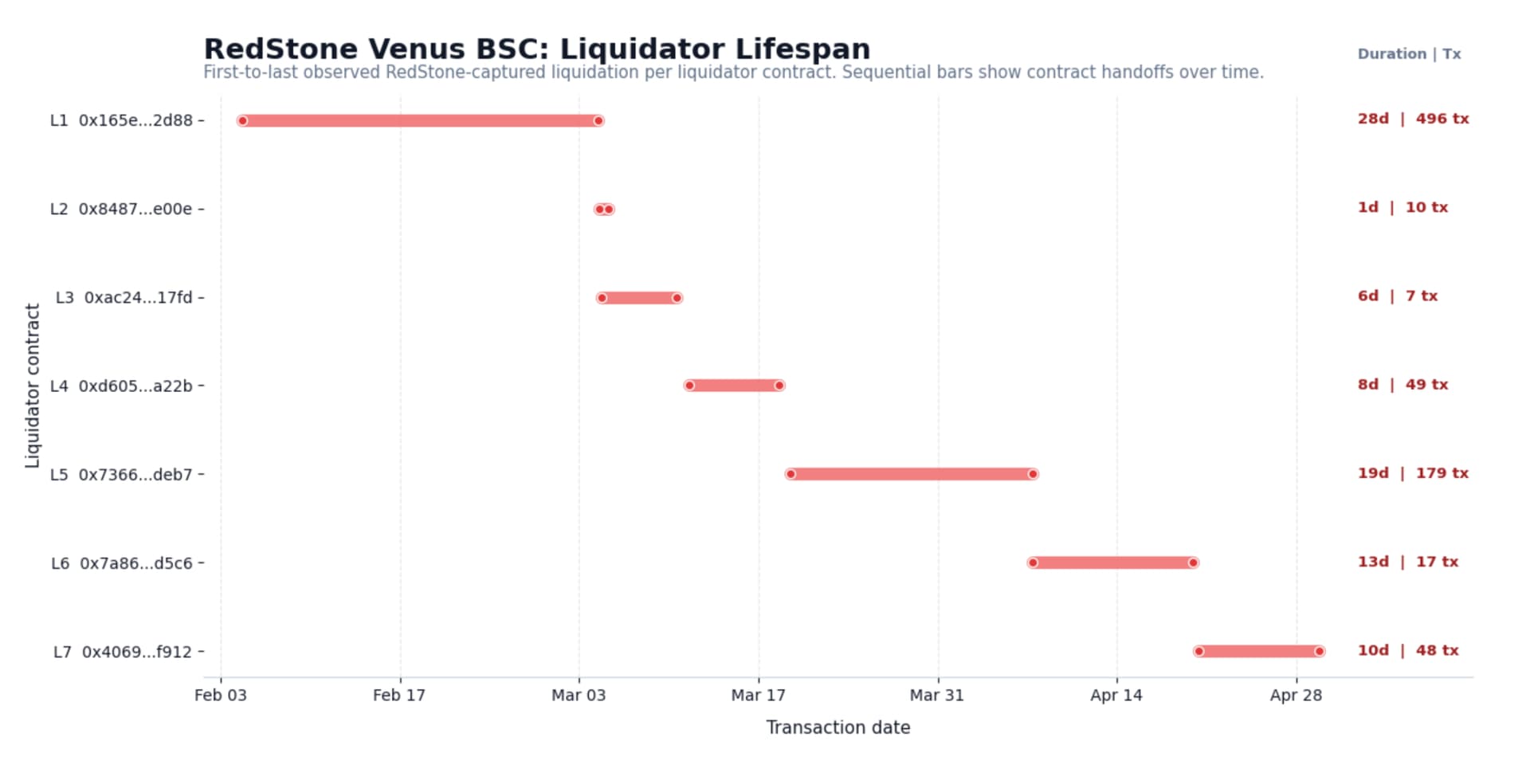

Observed liquidators, adjusted

Further Context

Chainlink SVR

During the trial period, Chainlink SVR saw 18 unique external solver contracts participate in auctions. Based on contract behavior and our operational knowledge of the ecosystem, we estimate these correspond to approximately 8–10 distinct liquidating entities. For conservatism in the comparison above, we report 8 active entities for SVR. We recognize that participant counts derived from on-chain activity warrant careful review, and we encourage the DAO and stakeholders to analyze the transaction history of the EOAs participating in SVR to validate that there are indeed many unique entities participating.

RedStone

Based on our on-chain observations, we observed only one liquidating entity associated with the RedStone setup throughout the entire trial period. All of the contracts that have performed liquidations for RedStone have been deployed by a single EOA; and none of the contracts overlapped with each other in activity. We did not observe evidence of the sort of broad auction participation seen in SVR. If RedStone’s operating model includes additional off-chain coordination that is not publicly visible, we encourage the team to describe that publicly so the DAO can evaluate the designs clearly.

[image]

Closing

Based on the observed trial results, we believe the choice for Venus should come down to which system has demonstrated the ability to deliver more value to the DAO, support broader liquidator participation, and remain dependable during periods of market stress. Chainlink SVR has shown that it can enable Venus to recapture more OEV while supporting the decentralized market structure that underpins long-term protocol resilience. We’re excited to continue improving SVR for Venus and ensure all Venus markets are powered by infrastructure built to perform when it matters most.

References and Documentation

- Chainlink SVR Announcement

- SVR Follow-up Research

- SVR Official Documentation

- SVR Performance Dashboard (LlamaRisk)

- Venus x Chainlink SVR Integration Proposal

- Venus Two-Vendor OEV Integration Framework