Terrence, despite asking for mods’ opinions on the matter, the team has ignored pretty much all the ideas from the feedback. From the feedback I listed 2 huge risks on cancelling VRT, which I would like to post it publicly and let all the community to read and reflect on, the first has already happened as predicted, and the second one will also happen in turn, with time progressing. Here is the copy & pasting from from the document I sent to Terrence on July 29th after admins and mods received the draft proposal from the team, which is exactly the same as the one posted.

THIS WILL BE A LONG READ BUT PLEASE GET TO THE BOTTOM FOR MATHS

VRT

VRT should take long-term development as the general direction, rather than completely abolishing the principal development.

The market risk of canceling VRT:

- The credibility crisis of Venus and the collapse of the community: After the liquidation incident on May 19, 2021, confidence in Venus has been weak, especially those who have been liquidated, they no longer have XVS. For maintaining the long-term vigorous development of the community, now cannot withstand another blow. Personally would prefer to retain the first wave of pioneers who participated in rise BSC and enhance the community effect of both BSC and Venus. The team has the responsibility to listen to the demands of the community, especially when the community’s voting results are very obvious. Otherwise, it is likely to affect the market’s confidence in the effective governance of Venus Protocol, hence the governance value of XVS. From a market perspective, the selling pressure from the community is likely to significantly affect the value of XVS in the short term. The international community generally has great hopes for VRT. Failure to implement what the former team promised may lead to a credibility crisis. I personally suggest that the update focuses on re-exploring the possibilities of programming, not about cancellation or redemption. - END OF FEEDBACK

By pushing the tokenomics as is, the community push back since the announcement was astronomical, the damage to the Venus brand and Binance Smart Chain as a whole, by simply pushing an unfavoured proposal, especially a proposal that clearly lost the vote, has been significant.

NOW THAT THE FIRST OF THE TWO SITUATION HAS HAPPENED, LET’S MOVE ON TO THE SECOND ONE WITH NUMBERS NOW.

- The continuous selling pressure brought to XVS by VRT swap and lock-up creates a potential psychological effect on future investors: The lock-up after the VRT purchase will release about 750,000 XVS to the market, which will affect the mentality of investors, plus the millions of XVS if VIP29 is implemented. XVS will face an additional burden lasting for 21-24 months. Although the quantity is still manageable, it still will affect the confidence of potential investor. If combining the effect with repurchase burning and dividends, the buyback and burn will not be as effective. The additional supply will have an impact on the value of XVS. - END OF FEEDBACK

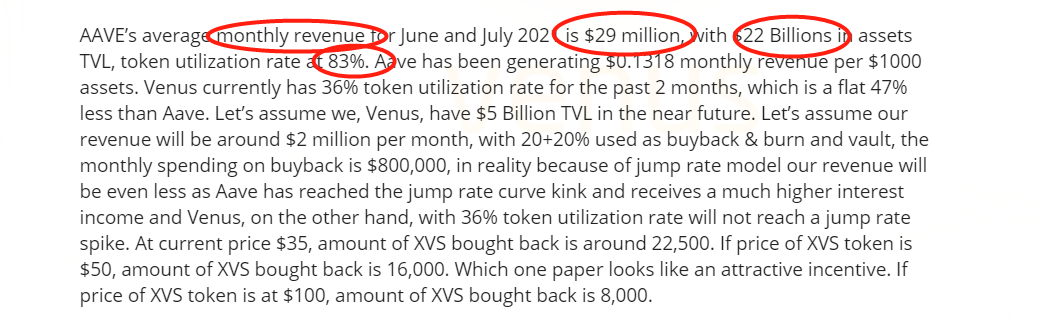

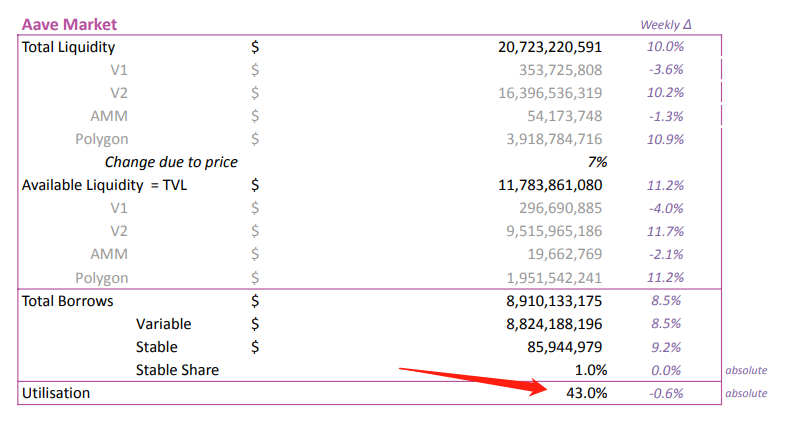

AAVE’s average monthly revenue for June and July 2021 is $29 million, with $22 Billions in assets TVL, token utilization rate at 83%. Aave has been generating $0.1318 monthly revenue per $1000 assets. Venus currently has 36% token utilization rate for the past 2 months, which is a flat 47% less than Aave. Let’s assume we, Venus, have $5 Billion TVL in the near future. Let’s assume our revenue will be around $2 million per month, with 20+20% used as buyback & burn and vault, the monthly spending on buyback is $800,000, in reality because of jump rate model our revenue will be even less as Aave has reached the jump rate curve kink and receives a much higher interest income and Venus, on the other hand, with 36% token utilization rate will not reach a jump rate spike. At current price $35, amount of XVS bought back is around 22,500. If price of XVS token is $50, amount of XVS bought back is 16,000. Which one paper looks like an attractive incentive. If price of XVS token is at $100, amount of XVS bought back is 8,000.

Our current emission through vaults is 8,500 per day, 255,000 per month. VRT vault exchange rate releases 64500 XVS into the market per month. VIP-29, assuming the average release price for XVS to settle bad debt is at $100, releases 770,000 XVS into the market over 9 months, which is around 85,000 per month.

We are facing an emission of 404,500 per month in the coming year, and yet our revenue buyback model is buying back anywhere between 10,000 to 20,000 per month, which is 5% or less compared to the total emission.

The team is pushing an tokenomics that would not benefit either XVS holder or VRT holder, while sugar coating it by not providing adequate mathematical calculations and market projections.

Without VRT replacing majority of daily emission for XVS, which is the biggest component of emission of XVS in the coming year, the tokenomics proposal hurts ALL token holders, regardless of whether we are a believer or single-token economy or dual-token economy.

With the implementation of VRT as rewards and slashing most of the supply of XVS through daily emission and keeping XVS emission low around 10 million, XVS has it’s highest potential fulfilled. Because of low XVS emission, buyback execution will have higher effect on the value of the token.

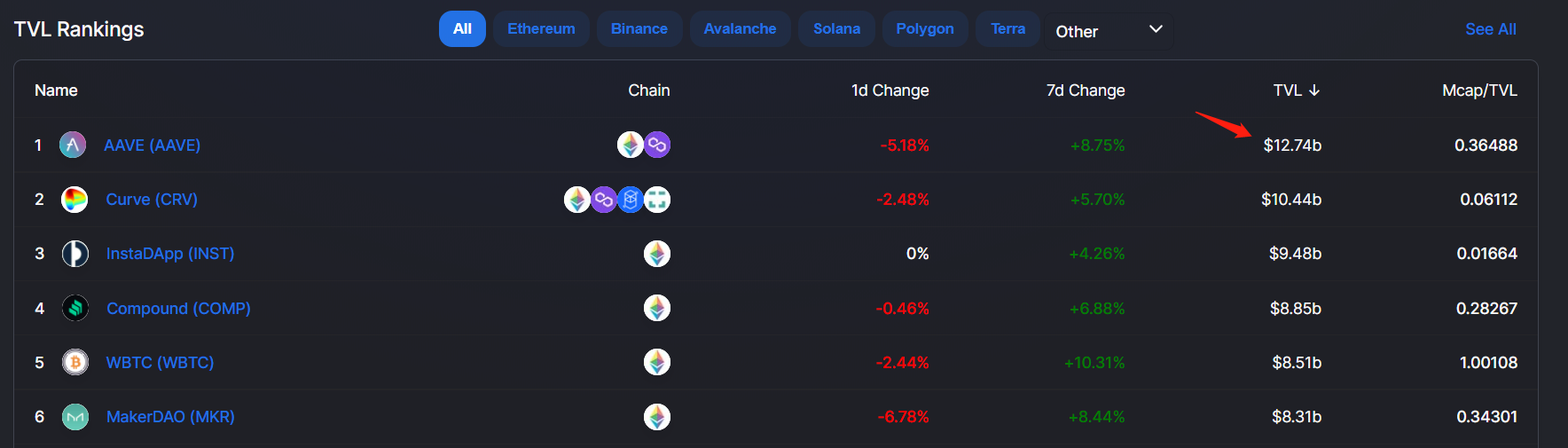

Let’s do a case study, MakerDAO has 8.3 Billion TVL right now at the moment the comment is written. The price of MKR token is $3131.50. The circulating supply is 991328 and there is no emission. By keeping XVS token supply around 10 million through low emission and effective buybacks, theoretically when Venus TVL reaches 8.3 Billion, the price of XVS token is at $313.

Of course market has a lot of variants and the case of MakerDAO and MKR token cannot be exactly replicated for Venus and XVS token. However, we can have an expected range of $200-$400 for the Venus token with it’s superior tokenomics compared to MKR token. The only way to achieve it, is to have a low XVS emission through VRT, and a vibrant community that trusts the team and is self-starting to promote the project for the project.