Recommendations From Gauntlet:

Summary

-

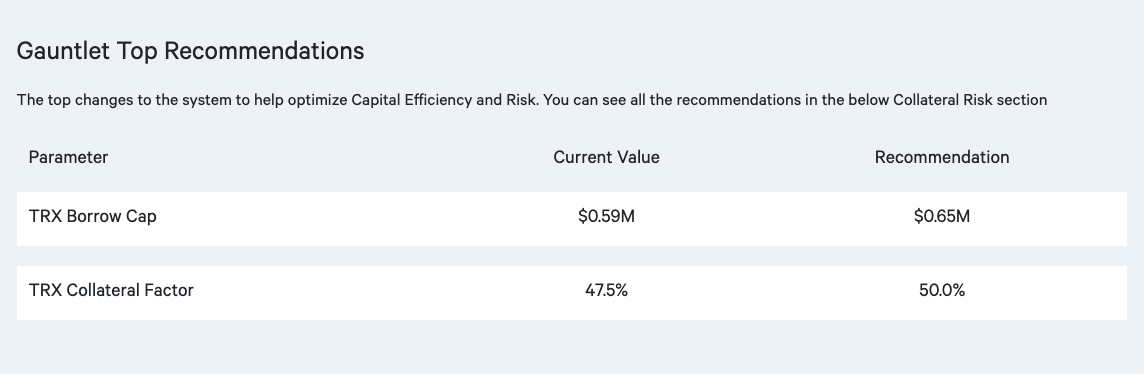

TRX:

- Increase borrow cap to 10m tokens from 9m

- Increase supply cap to 12m tokens from 11m

- Increase CF to 0.50 from 0.475

-

SXP:

- Wait for SXP suppliers to continue unwinding their positions

-

XVS:

- Continue to monitor the price of XVS

-

CAKE:

- Monitor CAKE market developments

Rationale

For the listed assets, Gauntlet recommends the following:

-

TRX:

- To encourage continued usage of TRX instead of TRXOLD, we recommend raising borrow and supply caps to 10,000,000 and 12,000,000 respectively, as well as raising the collateral factor to 0.50. With TRX market data accumulating, our models indicate that the liquidity of TRX warrants borrow and supply cap increases that introduce minimal additional risk to Venus. We note that TRX’s 2% depth across all CEX and DEX sources is $25m (~350m tokens). The top 3 wallets on Binance chain hold ~263m TRX, and the top 5 wallets hold ~273m TRX. We calculate these increases in borrow/supply caps will contribute about $3,053 of additional potential reserve fee revenue annually to Venus. We also assess the risk of price manipulation with respect to collateral factor, borrow cap, and supply cap recommendations. Increasing the collateral factor from 0.475 to 0.50 continues to incentivize utilize TRX, without introducing additional meaningful risk.

-

SXP:

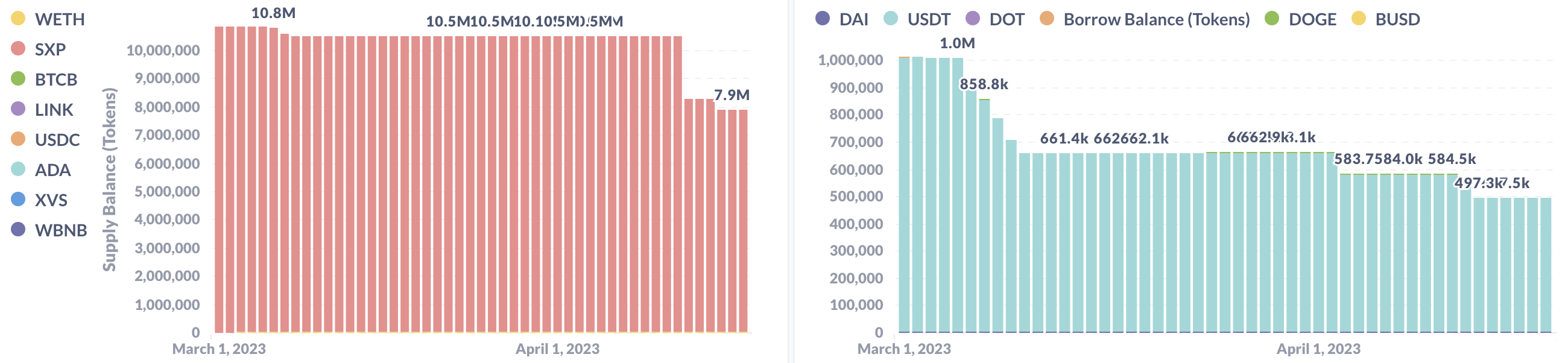

- While SXP is being deprecated from Venus, the two largest suppliers of SXP (addresses ending

34cfb4f1and068e9790) have lowered both their SXP (left charts) and their respective borrows (right charts). See the charts below (y-axis represents token amounts).

- While SXP is being deprecated from Venus, the two largest suppliers of SXP (addresses ending

- At SXP’s current price, the users are safe from being liquidated until SXP declines by at least 22%. If Venus lowered SXP’s CF now to 10%, the users would be close to being liquidated. Since the users are in the process of winding down their positions, we recommend allowing them more time before reducing SXP’s CF further.

-

XVS:

- After XVS spiked on April 9, 2023, the community voted to lower XVS’s CF to 0.55 from 0.60 to discourage users from utilizing their increased borrowing power, which could have negatively affected users if XVS quickly declined thereafter. Some users did indeed increase their borrow usage, including the largest XVS supplier (address ending

…5567078e), who had shown similar behavior previously in response to rises in XVS’s price (like when XVS rose 67.8% this year from Jan 1 through Feb 20). XVS remains at somewhat elevated levels (~$6.15) but has been declining since April 14. The top 20 XVS suppliers now have a weighted average borrow usage of ~57%. - The supply balance of XVS is currently at 99.9% of its supply cap of 1m, but given that the price of XVS has been declining since April 14, we recommend no changes and Gauntlet will continue to monitor before making any parameter changes. If XVS’s price stabilizes over a period of about 2 weeks, we would consider re-adjusting parameters for XVS.

- After XVS spiked on April 9, 2023, the community voted to lower XVS’s CF to 0.55 from 0.60 to discourage users from utilizing their increased borrowing power, which could have negatively affected users if XVS quickly declined thereafter. Some users did indeed increase their borrow usage, including the largest XVS supplier (address ending

-

CAKE:

- We’d like to note some recent developments with CAKE on Venus. First, a single user (account ending

...b5e1061b) supplied ~$6.3m of CAKE on April 22, 2023, borrowing around $3.8m in BNB. On the same day, another user (account ending...79ddfeaa) supplied around $2.4m CAKE (no borrows). The supply balance of CAKE on Venus accordingly spiked, peaking at around 95% of the supply cap (7m) on April 22, and sitting at around 90% supply cap usage as of April 24. Notably, CAKE’s price has declined 13.5% to around $2.90 on April 24 as well. Given this recent volatility of CAKE, we do not recommended changing its parameters on Venus at the moment, but we will continue to monitor the situation as it develops.

- We’d like to note some recent developments with CAKE on Venus. First, a single user (account ending

General Update

Below we provide a broader update on Venus protocol’s risk metrics.

1. Methodology

Gauntlet’s parameter updates seek to maintain the overall risk tolerance of the protocol while making risk trade-offs between specific assets.

Gauntlet’s parameter recommendations are driven by an optimization function that balances 3 core metrics: insolvencies, liquidations, and borrow usage. Parameter recommendations seek to optimize for this objective function. Our agent-based simulations use a wide array of varied input data that changes daily (including but not limited to asset volatility, asset correlation, asset collateral usage, DEX / CEX liquidity, trading volume, the expected market impact of trades, and liquidator behavior). Gauntlet’s simulations tease out complex relationships between these inputs that cannot be expressed as heuristics. As such, the input metrics we show below can help explain why some of the param recs have been made but should not be taken as the only reason for the recommendation. The individual collateral pages on the Venus Risk Dashboard cover other vital statistics and outputs from our simulations that can help with understanding interesting inputs and results related to our simulations.

For more details, please see Gauntlet’s Parameter Recommendation Methodology and Gauntlet’s Model Methodology.

2. Risk Dashboard

The community should use Gauntlet’s Venus Risk Dashboard to understand better any updated parameter suggestions and general market risk in Venus. Value at Risk represents the 95th percentile insolvency value that occurs from simulations we run over a range of volatilities to approximate a tail event. Liquidations at Risk represents the 95th percentile liquidation volume that occurs from simulations we run over a range of volatilities to approximate a tail event. We would note that our methodology on borrow/supply caps is currently driven by risk modeling that is independent and additive to our risk simulations shown on the Dashboard.

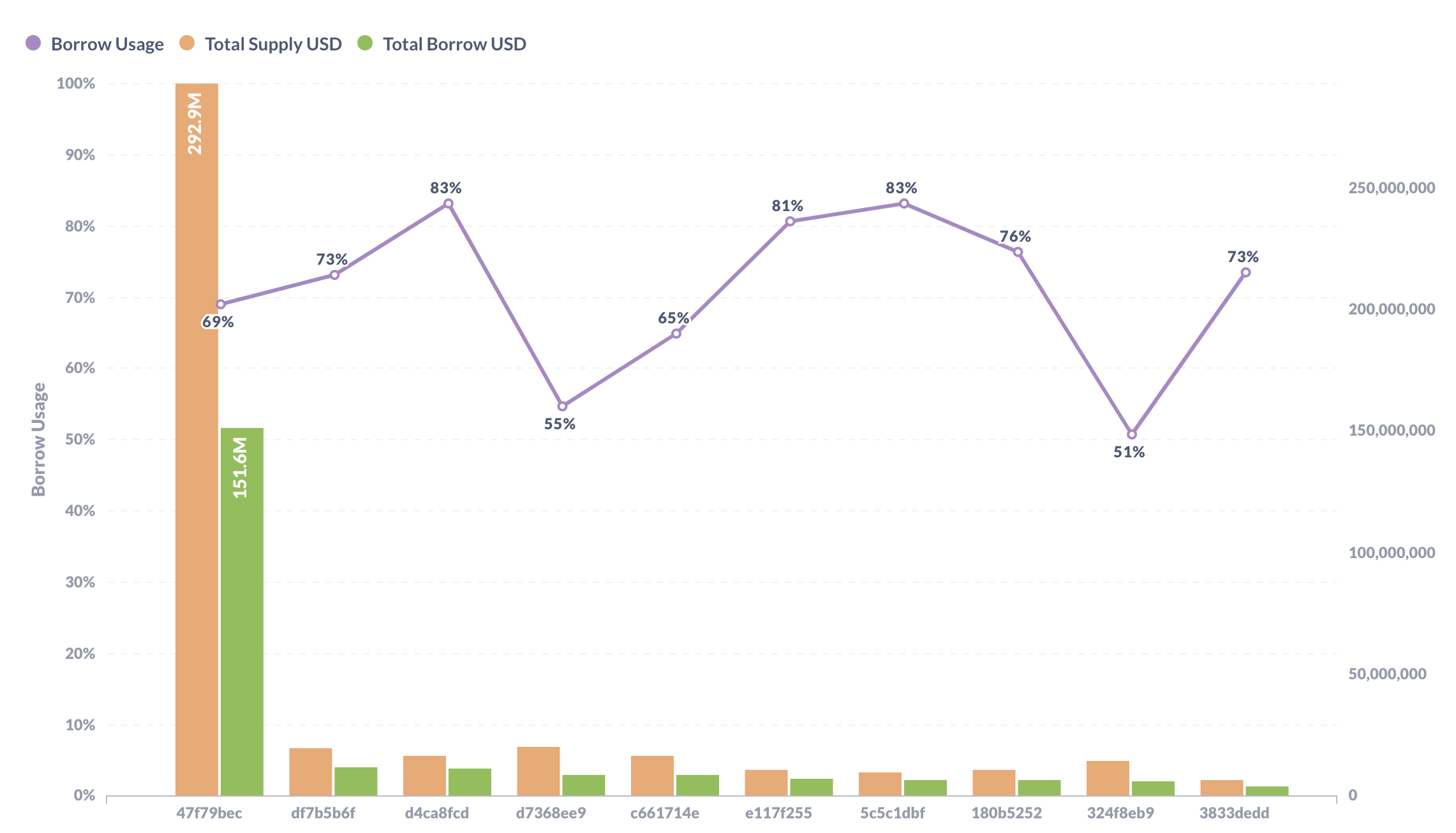

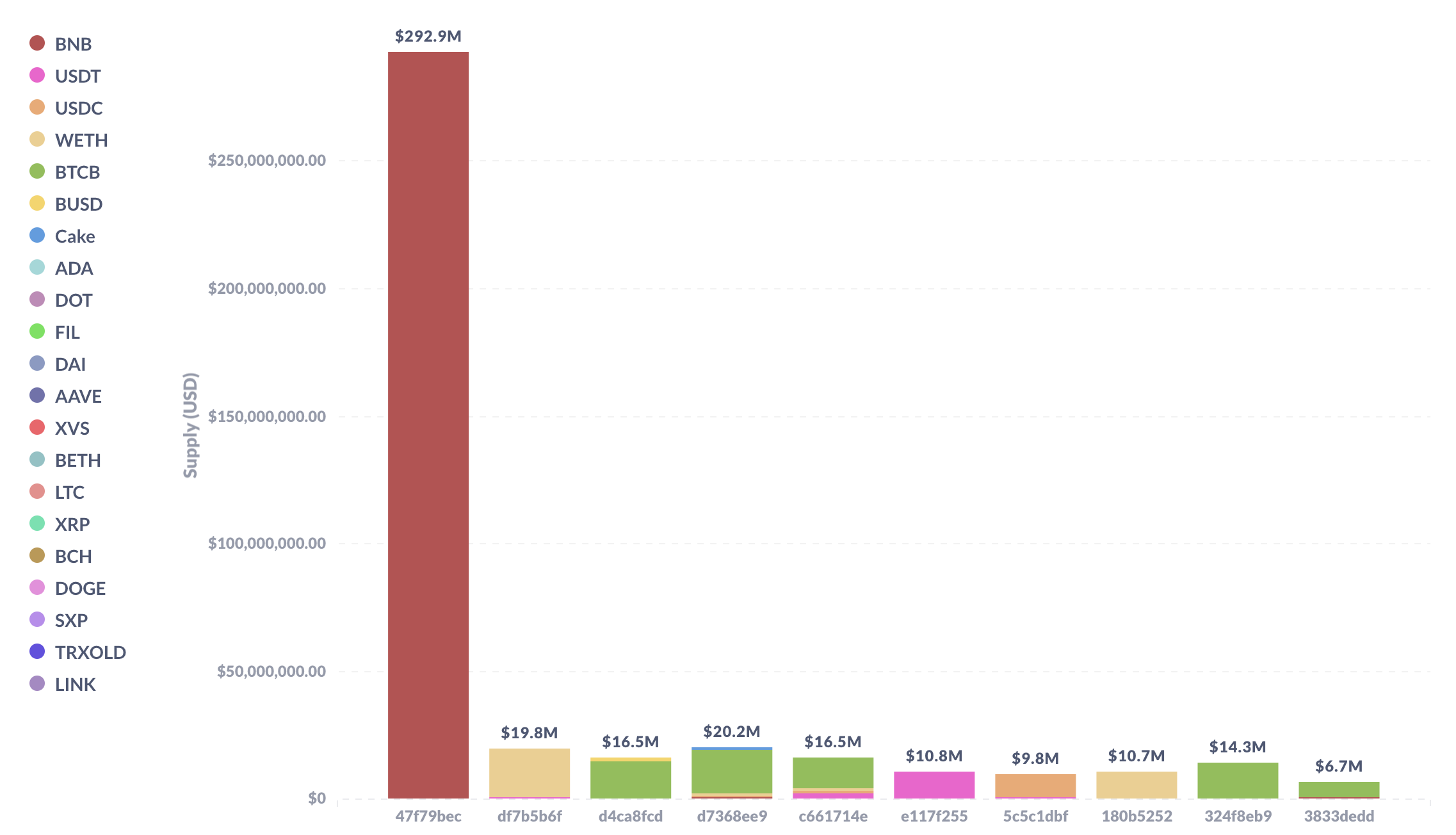

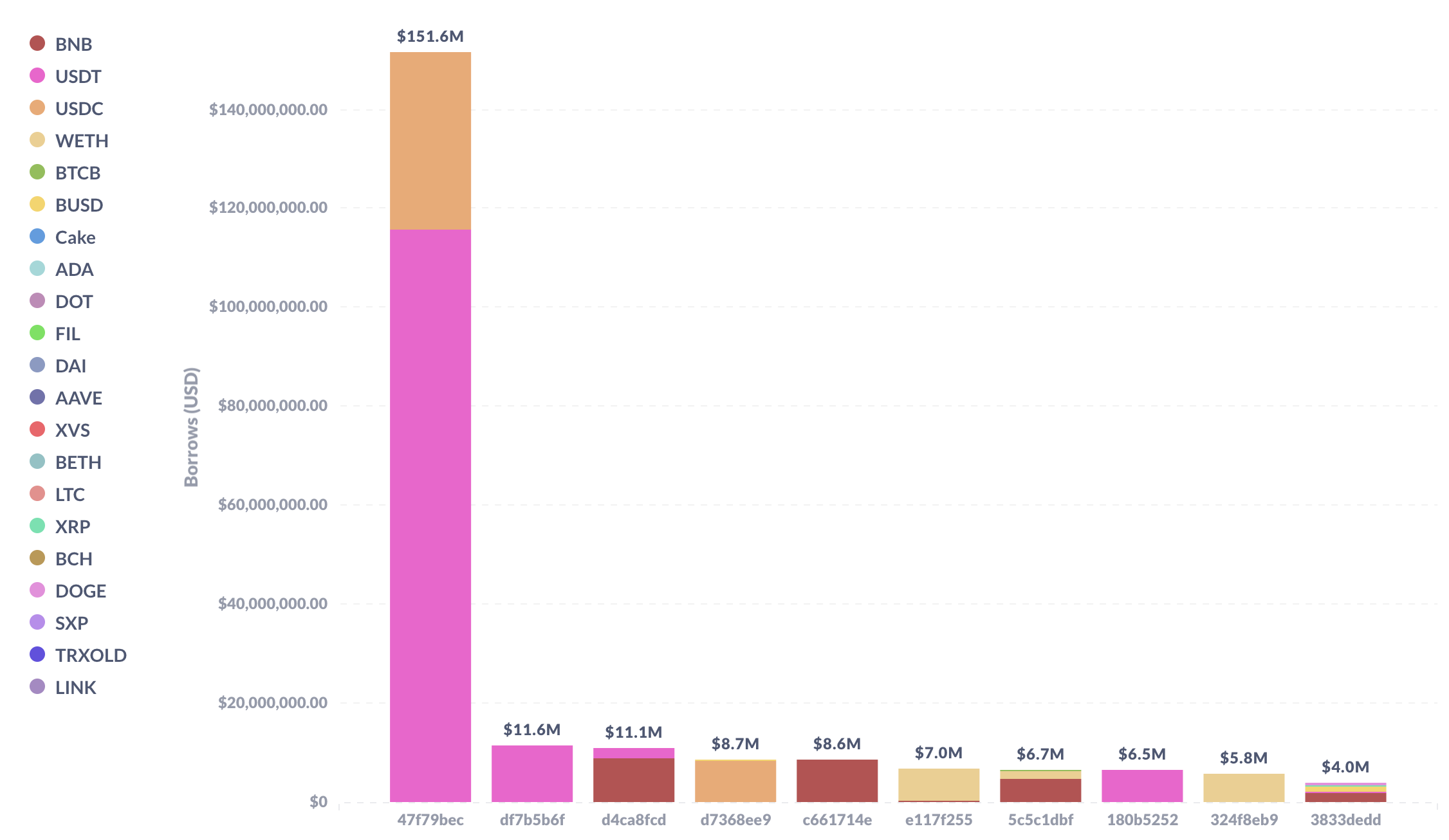

3. Top Borrowers

The below figures show trends in key market statistics regarding borrows and utilization that we will continue to monitor:

Top 10 Borrowers’ Aggregate Positions & Borrow Usages

Top 10 Borrowers’ Entire Supply

Top 10 Borrowers’ Entire Borrows

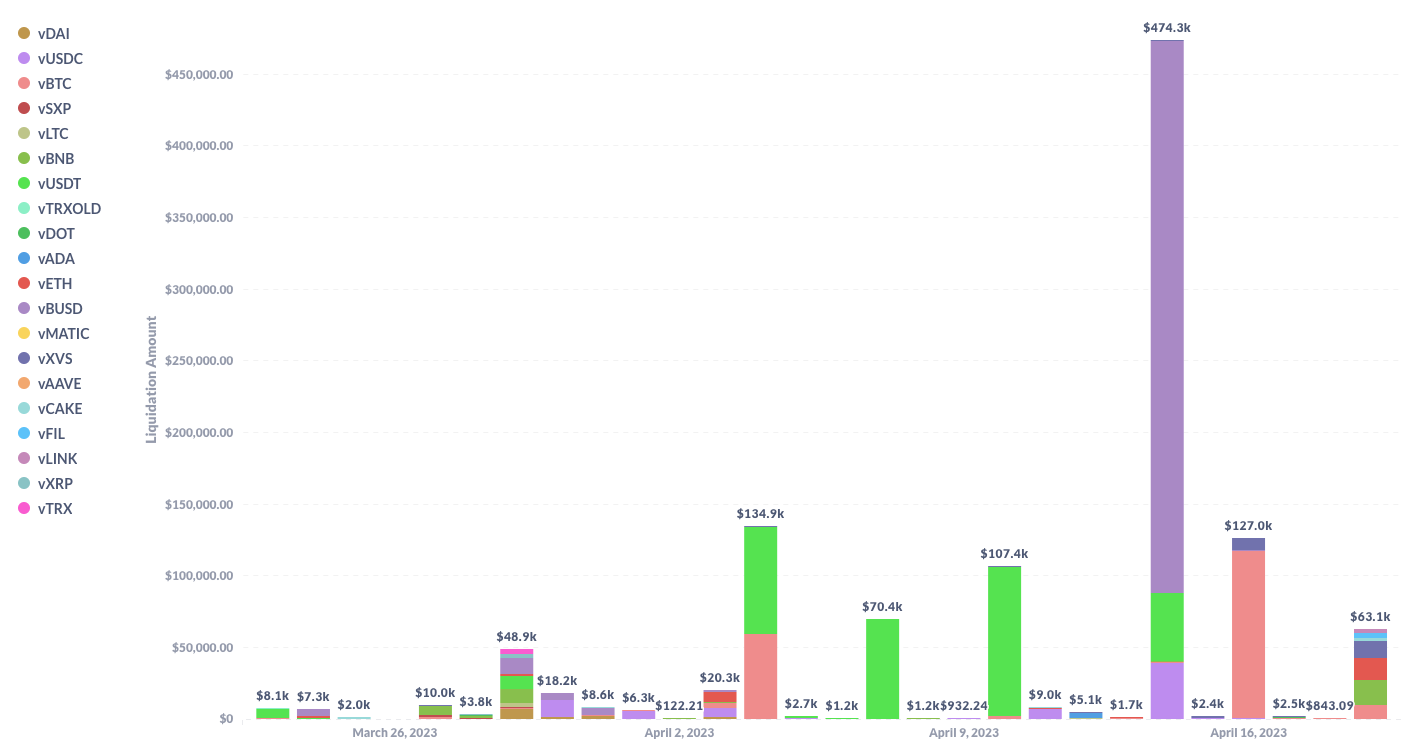

4. Liquidations

As Gauntlet tracks the state of the market and protocol, the charts below show some of the behavior we have been monitoring to ensure minimal market risk.

- April 4: Liquidations of $74.4k and $59.7k, totaling ~$135k, occurred on April 4. The former liquidation resulted from the borrowed asset, DOGE, experiencing a price spike of ~33% from April 3 to April 4. The latter liquidation, which borrowed ETH, was liquidated due to a 6% increase in ETH price on April 4.

- April 10: A single user liquidation of $104.2k occurred on April 10. This user posted USDT as collateral to borrow WBNB and was liquidated as a result of a 3% increase in the price of WBNB on April 10.

- April 14: Venus saw a total of $474.3k in liquidation volume on April 14. The majority of this total is comprised of three individual user liquidations that borrowed ETH and were liquidated as a result of its 11% price increase on April 14. The three users were liquidated for $47.4k (supplied USDT), $231.7k (supplied BUSD), and $145.1k (supplied BUSD) respectively, totaling $424.5k of the total $474.3k liquidation volume for that day. One other liquidation of $36.1k occurred on April 14 for a user that borrowed BTCB and supplied USDC and was liquidated due to BTCB’s 14% price increase that day.

- April 16: Venus saw a total of $127k in liquidation volume on April 16, mainly comprised of two user liquidations of $64.2k and $52.7k. Both users borrowed ETH and supplied BTC, and were similarly liquidated as a result of ETH’s additional 3% price increase between April 14 and April 16.

We will continue to monitor user and protocol positions and make recommendations as needed. The charts below show the liquidations and repaid borrows of accounts liquidated in the past month.

Liquidations

Repaid Borrows

Next Steps:

- These recommendations will be put up for a VIP vote

By approving this proposal, you agree that any services provided by Gauntlet shall be governed by the terms of service available at gauntlet.network/tos.