Venus Parameter Recommendations 2022-12-01

Gauntlet makes the following recommendations to optimize risk and capital efficiency for Venus:

Summary Recommendations

CF:

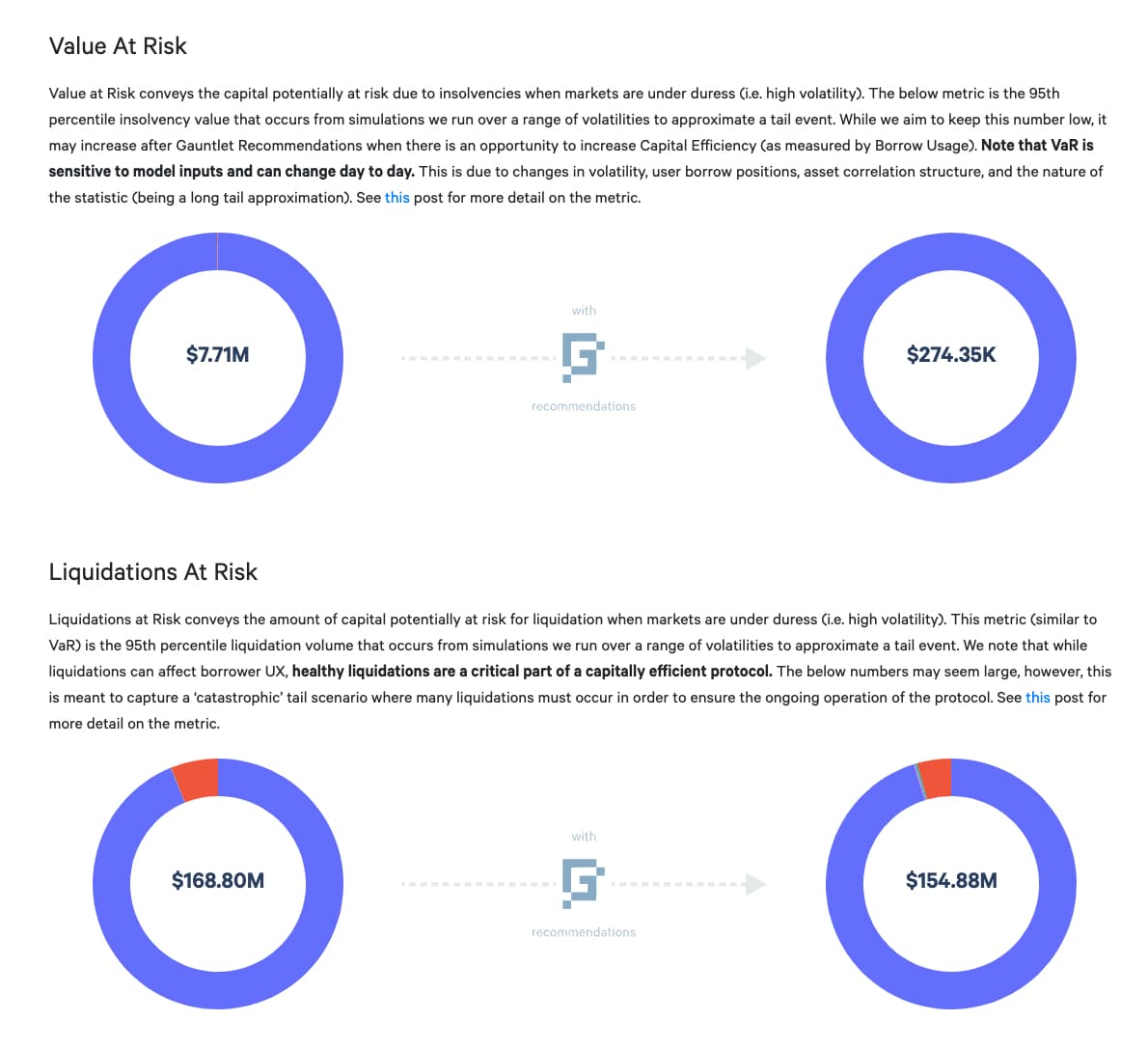

- We recommend decreasing BNB collateral factor from 80% to 75%. This would reduce the Value at Risk (VAR) for Venus from $7.7m → $270k to minimize risk for “Black Thursday” events.

Supply Caps and Borrow Caps (denominated in TOKEN NOT USD):

| Symbol | Current Supply Cap | Current Borrow Cap | VIP 77 supply caps | Recommended Supply Cap | Recommended Borrow Cap |

|---|---|---|---|---|---|

| USDT | - | - | - | 736,300,000 | 245,500,000 |

| XVS | - | 0 | - | 1,311,000 | 0 |

| XRP | - | - | 1,000,000,000 | 35,400,000 | 3,029,000 |

| USDC | - | - | - | 258,000,000 | 124,700,000 |

| TUSD | - | - | - | 21,130,000 | 11,810,000 |

| TRX | - | - | - | 48,300,000 | 16,400,000 |

| SXP | - | - | 25,000,000 | 25,000,000 | 6,410,000 |

| MATIC | - | - | 262,000,000 | 6,718,000 | 1,470,000 |

| LTC | - | - | 2,000,000 | 254,100 | 25,410 |

| LINK | - | - | 15,000,000 | 2,388,000 | 238,800 |

| FIL | - | - | 9,000,000 | 908,500 | 122,200 |

| ETH | - | - | - | 222,300 | 28,740 |

| DOT | - | - | 33,000,000 | 2,209,000 | 776,400 |

| DOGE | - | - | 4,000,000,000 | 157,700,000 | 23,240,000 |

| DAI | - | - | - | 13,910,000 | 5,414,000 |

| CAKE | - | 2,500,000 | 7,000,000 | 7,000,000 | 3,749,000 |

| BUSD | - | - | - | 680,800,000 | 184,500,000 |

| BTCB | - | - | - | 22,770 | 3,531 |

| BNB | - | - | - | 2,672,000 | 2,008,000 |

| BETH | - | - | - | 21,890 | 16,450 |

| BCH | - | - | 500,000 | 26,820 | 4,331 |

| ADA | - | - | 1,000,000,000 | 37,510,000 | 14,430,000 |

| AAVE | - | - | 422,000 | 19,160 | 4,808 |

Methodology

This set of parameter updates seeks to maintain the overall risk tolerance of the protocol while making risk trade-offs between specific assets.

Gauntlet’s parameter recommendations are driven by an optimization function that balances 3 core metrics: insolvencies, liquidations, and borrow usage. Parameter recommendations seek to optimize for this objective function. Our agent-based simulations use a wide array of varied input data that changes on a daily basis (including but not limited to asset volatility, asset correlation, asset collateral usage, DEX / CEX liquidity, trading volume, expected market impact of trades, and liquidator behavior). Existing insolvencies are excluded from our simulations and VaR and LaR numbers. Gauntlet’s simulations tease out complex relationships between these inputs that cannot be simply expressed as heuristics. As such, the input metrics we show below can help understand why some of the param recs have been made but should not be taken as the only reason for recommendation. The individual collateral pages on the Gauntlet’s Venus Risk Dashboard cover other key statistics and outputs from our simulations that can help with understanding interesting inputs and results related to our simulations.

For more details, please see Gauntlet’s Parameter Recommendation Methodology 1 and Gauntlet’s Model Methodology 1.

Risk Off Liquidations:

Whenever we lower collateral factors, there’s a chance that some users may immediately become liquidatable as a result. There are a number of accounts that lend and borrow stablecoins and keep their balances just slightly above the liquidation threshold.

Reducing the collateral factor of BNB by 5% would push 90 accounts from

just above the collateral factor to just below the collateral factor. The accounts have a total borrow value of $165k. The top account has a borrow balance of $150k. Most of the accounts are extremely small.

Supply Caps and Borrow Caps:

In light of the recent abnormal liquidations and activity across many lending protocols, Gauntlet recommends conservative borrow and supply caps on all assets, particularly on those who have low liquidity and/or supply on BSC, in order to significantly lower the potential for price manipulation. Over time, as the Venus lending market grows for many of these assets, we will continue to monitor these parameters and recommend adjustments as needed.

Supporting Data

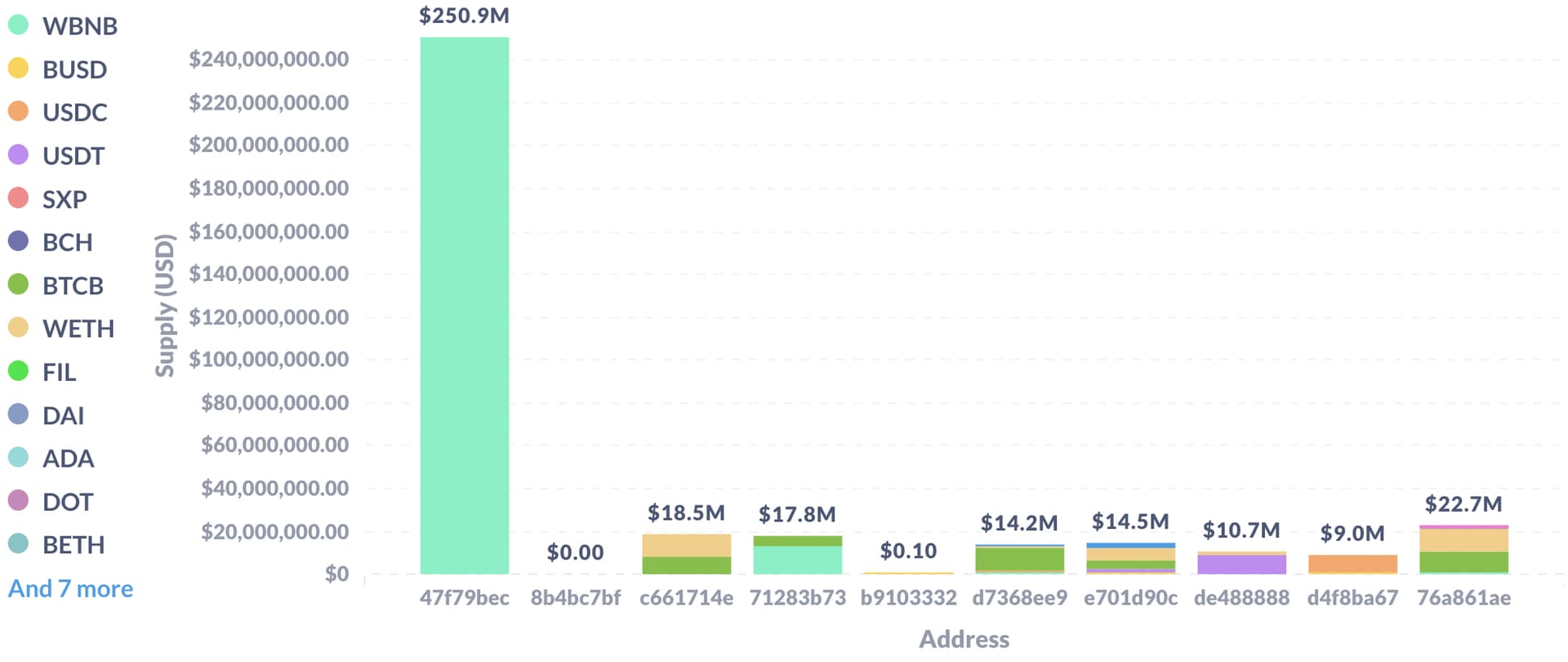

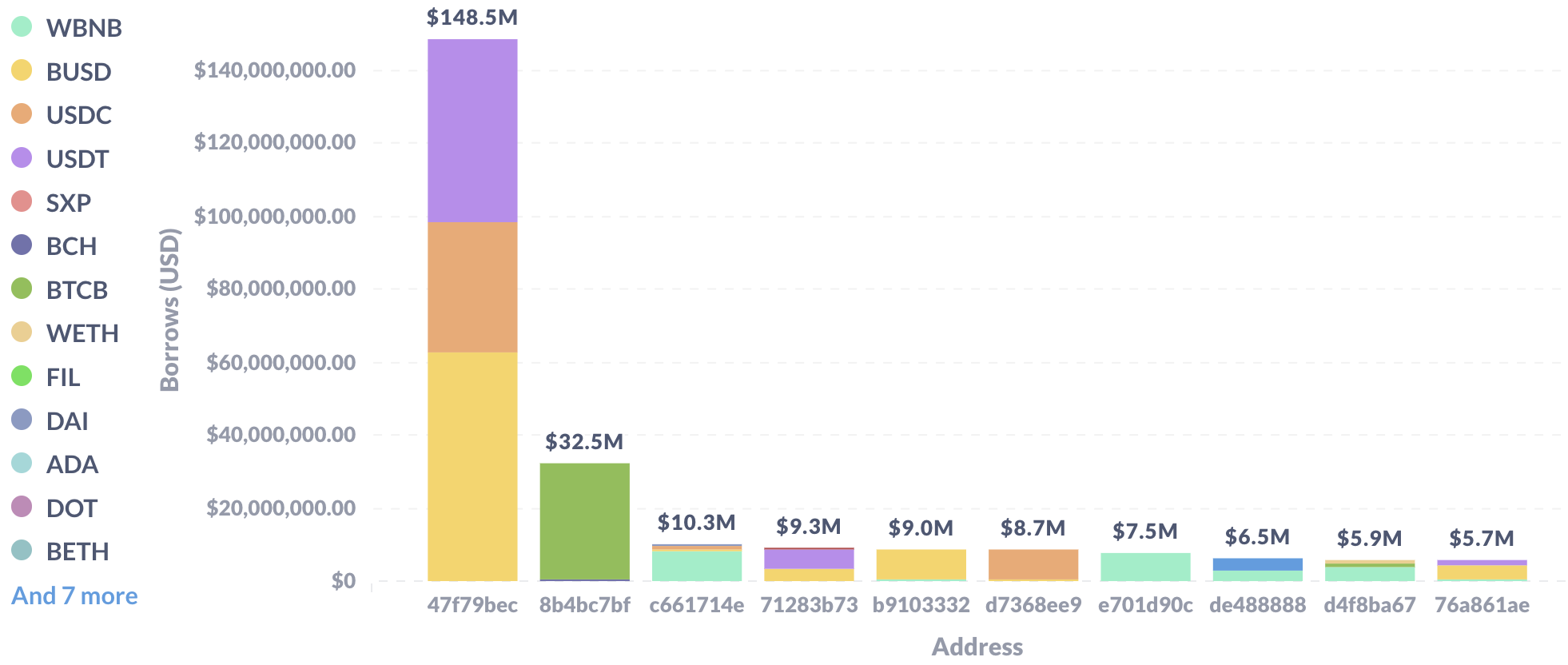

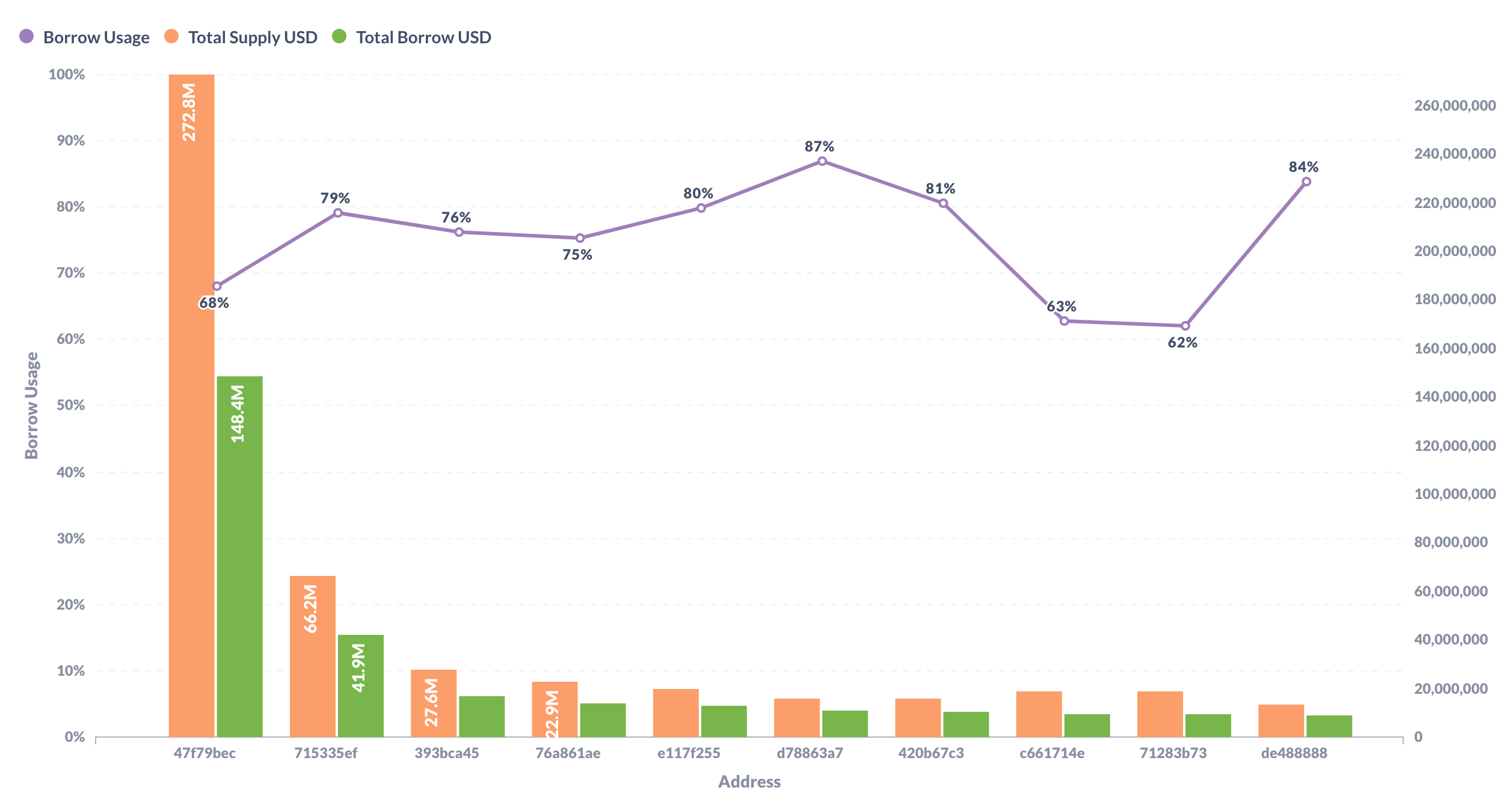

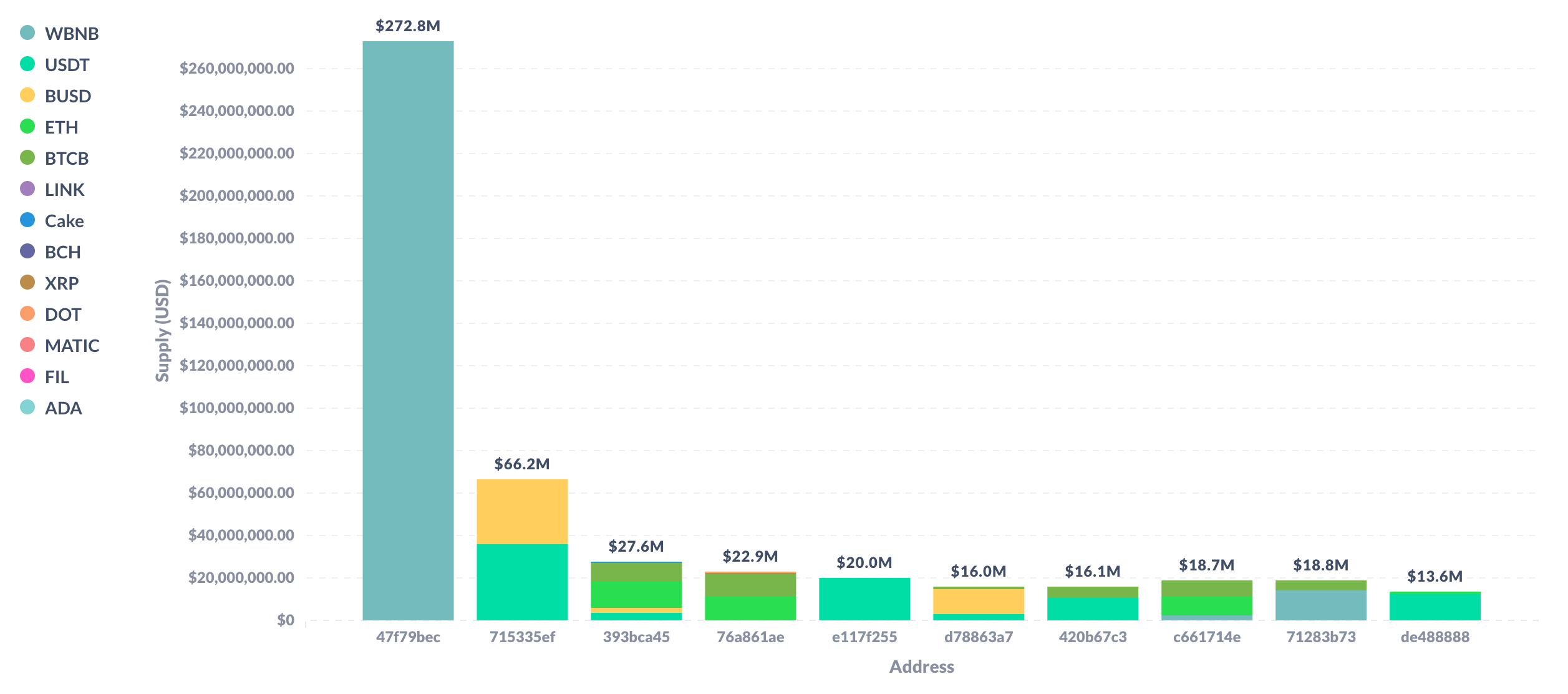

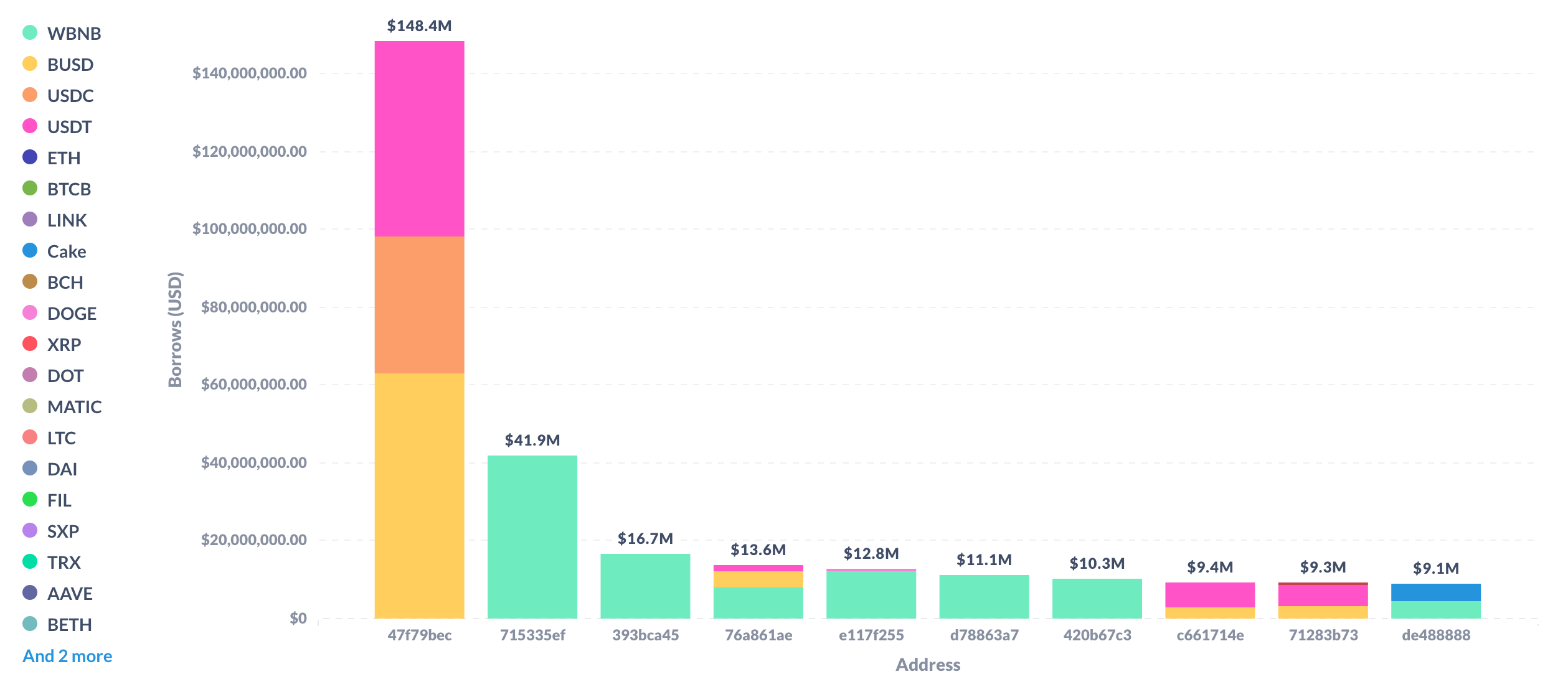

Top 10 borrowers, Aggregate Positions and Borrow usages

Top 10 borrowers, Breakdown of Borrower Supply

Top 10 Borrowers Breakdown of Borrows

Above shows the distribution in risk among the top borrowers - A large amount of BNB is concentrated in one borrower, which could lead to insolvencies. Because of this, we can observe why a large portion of the VaR is in BNB.

Risk Dashboard

The community should use Gauntlet’s Venus Risk Dashboard to better understand the updated parameter suggestions and general market risk in Venus.

Value at Risk represents the 95th percentile insolvency value that occurs from simulations we run over a range of volatilities to approximate a tail event.

Liquidations at Risk represents the 95th percentile liquidation volume that occurs from simulations we run over a range of volatilities to approximate a tail event.

Next Steps

- Gauntlet to put up a snapshot vote for the community to vote on

so we will need probably to discuss positive vs negative for each change in the parameter of individual assets.

so we will need probably to discuss positive vs negative for each change in the parameter of individual assets.

For higher TVL,

For higher TVL,

the only thing i wanted to say is that for example in last Binance launchpad we earned about 2.500 BNB cuz supply APY was in range between 50-60% mostly with zero or minimum liquidity. If we will use same example with your proposed caps (they are almost 2x higher so our launchpad profit would be approx 5.000 BNB) but your caps means that we can borrow only 75% of supplied BNB and with our jump rate model if BNB supply increases to the maximum cap during the next launchpad and there will be a borrow cap of 75% APY on BNB market will be max. 5.53% instead of 50-60% so instead of 5.000 BNB our profit will be around 500 BNB and that is of course a huge difference, especially if we consider some future Bull market phase.

the only thing i wanted to say is that for example in last Binance launchpad we earned about 2.500 BNB cuz supply APY was in range between 50-60% mostly with zero or minimum liquidity. If we will use same example with your proposed caps (they are almost 2x higher so our launchpad profit would be approx 5.000 BNB) but your caps means that we can borrow only 75% of supplied BNB and with our jump rate model if BNB supply increases to the maximum cap during the next launchpad and there will be a borrow cap of 75% APY on BNB market will be max. 5.53% instead of 50-60% so instead of 5.000 BNB our profit will be around 500 BNB and that is of course a huge difference, especially if we consider some future Bull market phase.  If you understand me i know that with our actual supply and borrow nothing changes, our profit would be the same but if supply will growth fast to maximum during Launchpads we will lost millions of USD (in BNB tokens) in a few weeks. So I’m not sure if this is the best solution for us. And that’s not counting the reduction of CF at BNB from 80% to 75%, which is another significant loss of revenue.

If you understand me i know that with our actual supply and borrow nothing changes, our profit would be the same but if supply will growth fast to maximum during Launchpads we will lost millions of USD (in BNB tokens) in a few weeks. So I’m not sure if this is the best solution for us. And that’s not counting the reduction of CF at BNB from 80% to 75%, which is another significant loss of revenue.