Summary

This proposal recommends adjusting XVS emissions on Ethereum Mainnet by reducing them by 36%, based on an analysis of TVL proportions and market sensitivity. Additionally, 77,853 XVS is requested for distribution over the next 4 months. The following table outlines the proposed emission adjustments:

| Pool | Market | New Monthly Allocation (Change) |

|---|---|---|

| Core | WETH | 633 (25%) |

| Core | WBTC | 1,898 (25%) |

| Core | USDT | 2,279 (25%) |

| Core | USDC | 2,279 (25%) |

| Core | crvUSD | 0 (100%) |

| Core | FRAX | 0 (100%) |

| Core | sFRAX | 0 (100%) |

| Core | TUSD | 0 (100%) |

| Core | DAI | 0 (100%) |

| Curve | CRV | 0 (100%) |

| Curve | crvUSD | 0 (100%) |

| LST ETH | ETH | 12,375 (25%) |

| LST ETH | wstETH | 0 (100%) |

| LST ETH | sfrxETH | 0 (100%) |

| Total | 19,464 (-36%) |

Details

Considerations

All prices and market TVLs are considered for Sept 12, 2024

TVL Analysis

The TVL participation for each market is analyzed to filter out the most significant markets. The goal is to identify markets that hold a significant portion of the total TVL and categorize them into two tiers.

- Tier 1: Markets with more than 3% in TVL

- Tier 2: Markets with less than 3% in TVL

The following table shows the TVL participation:

| Pool | Market | Supply Amount | Borrow Amount | TVL Proportion |

|---|---|---|---|---|

| LST ETH | WETH | $37,830,000 | $34,390,000 | 41.41% |

| LST ETH | wstETH | $24,430,000 | $20,390,000 | 25.70% |

| Core | WBTC | $12,350,000 | $7,740,000 | 11.52% |

| Core | USDT | $6,340,000 | $4,810,000 | 6.39% |

| Core | USDC | $7,220,000 | $5,080,000 | 7.05% |

| Core | WETH | $3,620,000 | $1,680,000 | 3.04% |

| Core | crvUSD | $1,310,000 | $957,033 | 1.30% |

| Core | TUSD | $1,000,000 | $802,010 | 1.03% |

| LST ETH | sfrxETH | $969,010 | $913,420 | 1.08% |

| Core | sFRAX | $505,760 | $301,230 | 0.46% |

| Core | FRAX | $398,440 | $271,440 | 0.38% |

| Core | DAI | $275,210 | $218,170 | 0.28% |

| Curve | crvUSD | $216,230 | $154,570 | 0.21% |

| Curve | CRV | $134,180 | $80,510 | 0.12% |

The Tier 1 markets identified are WETH, wstETH, WBTC, USDT, USDC, as they have more than 3% in TVL. All other markets fall into Tier 2.

Sensitivity Analysis

The sensitivity analysis aims to determine how responsive each market is to changes in emissions. This helps in understanding which markets are more sensitive and how they should be treated during emission adjustments.

The following table showcases the effects of the past emission adjustment on the TVL for specific markets:

| Market | Event | Supply Difference | Borrow Difference |

|---|---|---|---|

| vUSDC_Core | Emissions Decreased 1 August | 6.81% | 9.71% |

| vUSDT_Core | Emissions Decreased 1 August | 9.81% | 10.27% |

| vWBTC_Core | Emissions Decreased 1 August | 3.50% | 0.05% |

| vWETH_Core | Emissions Decreased 1 August | -0.88% | -0.72% |

| vWETH_LiquidStakedETH | Emissions Decreased 1 August | -0.10% | -0.30% |

| vwstETH_LiquidStakedETH | Emissions Decreased 1 August | 0.01% | 0.00% |

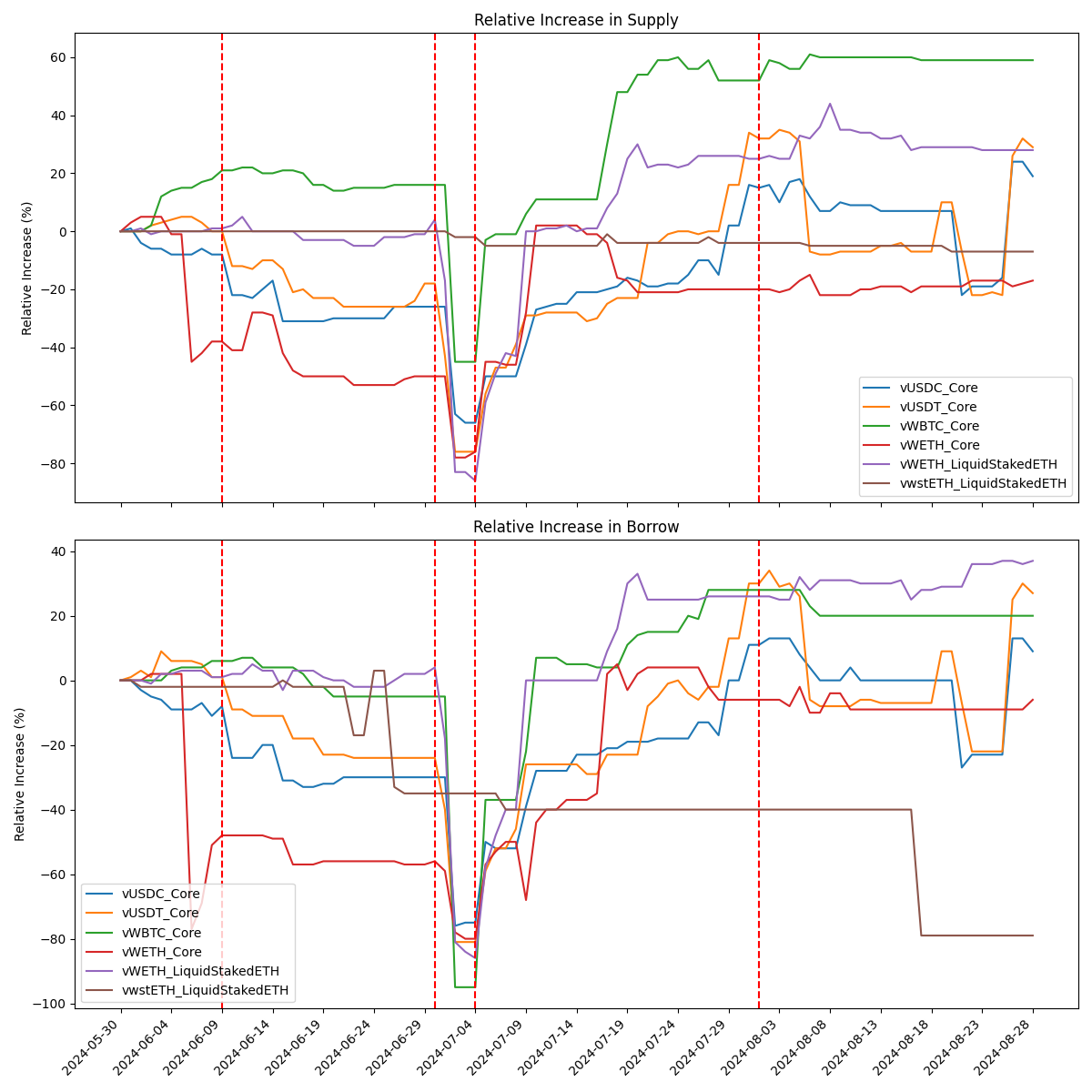

Graph of Sensitivity Analysis

Market sensitivity will be calculated by averaging the relative variation in TVL over 5 days before and after the change in emissions, based on the latest changes in emissions on August 1.

Market TVL Sensitivity to Emission Adjustments:

| Pool | Market | TVL Sensitivity to Emission Reductions |

|---|---|---|

| Core | WETH | -0.80% |

| Core | WBTC | 0% |

| Core | USDT | 0% |

| Core | USDC | 0% |

| LST ETH | ETH | -0.20% |

| LST ETH | wstETH | 0% |

- Note: An increase in TVL after the emission change is considered to have a sensitivity of 0, indicating no negative effects from the emission changes.

Final Recommendations

Following the August 1 adjustment, the impact on market TVL was minimal, with slight reductions of 0.8% in the ETH Core pool and 0.2% in the LST pool. Based on these results, the following recommendations are proposed:

-

Remove Emissions for Low TVL Markets:

Eliminate emissions for markets with less than 3% TVL participation due to their minimal contribution.

-

Remove LST Market Emissions:

LST markets, like wstETH, showed negligible response to emission changes, supporting the removal of their emissions.

-

Replicate August 1 Adjustments:

Since the August 1 adjustments had minimal impact, apply the same approach to the protocol’s most significant tokens.

| Pool | Market | Current Monthly Allocations | Adjustment | New Allocation |

|---|---|---|---|---|

| Core | WETH | 844 | 25% | 633 |

| Core | WBTC | 2,531 | 25% | 1,898 |

| Core | USDT | 3,038 | 25% | 2,279 |

| Core | USDC | 3,038 | 25% | 2,279 |

| Core | crvUSD | 750 | 100% | 0 |

| Core | FRAX | 300 | 100% | 0 |

| Core | sFRAX | 300 | 100% | 0 |

| Core | TUSD | 100 | 100% | 0 |

| Core | DAI | 250 | 100% | 0 |

| Curve | CRV | 188 | 100% | 0 |

| Curve | crvUSD | 188 | 100% | 0 |

| LST ETH | ETH | 16,500 | 25% | 12,375 |

| LST ETH | wstETH | 1,800 | 100% | 0 |

| LST ETH | sfrxETH | 400 | 100% | 0 |

| Total | 30,227 | -36% | 19,464 |

This proposal will ask for XVS funding to support these incentives up to January 2025. The needed amounts per distributor are the following:

| Distributor | Monthly XVS Amount | Total XVS Amount for 4 Months |

|---|---|---|

| Core | 7,088 | 28,353 |

| Curve | 0 | 0 |

| LST | 12,375 | 49,500 |

| Total | 19,464 | 77,856 |