Overview

Following the recommendation for the sUSDe/USDe Stablecoin Pool on the Venus BNB instance, Chaos Labs proposes expanding the pool to include USDT, USDC, and PT-USDe-30OCT2025. We believe this will further enhance capital efficiency without adding risk. In this post, we outline our analysis of the E-mode and the listing of PT-USDe-30OCT2025.

USDT & USDC E-Mode

We recommend adding USDT and USDC into the stablecoin E-Mode as debt assets. This inclusion does not introduce additional risk. Both USDT and USDC have long-established track records, dominant market share, and deep liquidity across centralized and decentralized venues on BNB. Their pegs to the U.S. dollar are reinforced by reserve backing and active arbitrage, which also ensures strong alignment with USDe. As a result, repayment exposure remains in the same dollar-pegged risk category, preserving the integrity of the E-Mode design.

At the same time, this addition enhances capital efficiency. Currently, USDT is the largest debt asset against sUSDe in the Venus BNB Core Pool, accounting for 72% of total outstanding debt. Furthermore, PT-USDe is expected to be used primarily as collateral to borrow USDe, USDT, and USDC in looping strategies. Allowing USDT and USDC as borrowable assets within E-Mode significantly improves efficiency for users and can drive growth of the instance. Because of the alignment between USDT, USDC, and USDe, along with USDe’s structural linkage to PT-USDe and sUSDe, systemic risk remains controlled.

PT-USDe-30OCT2025

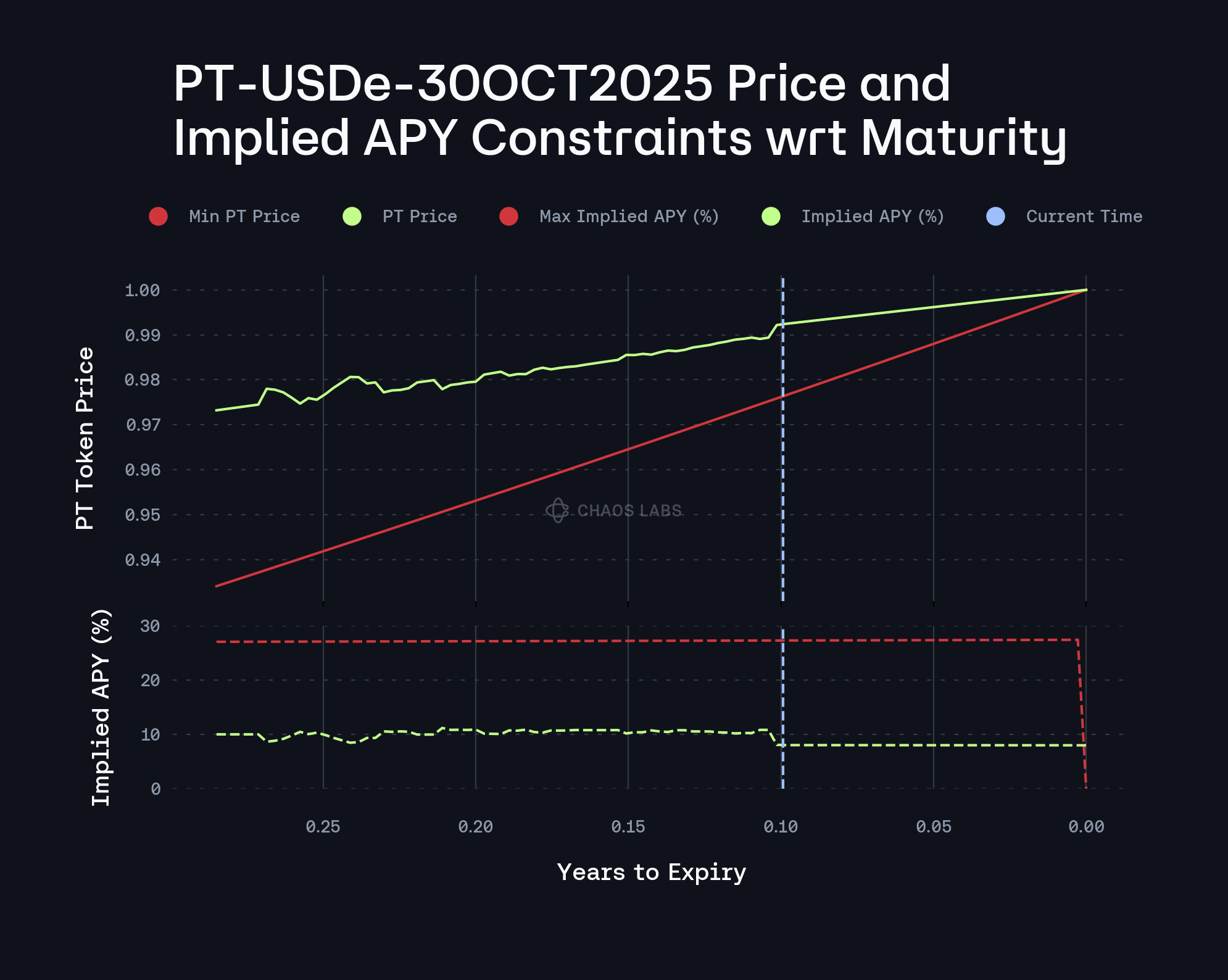

In parallel, we recommend adding PT-USDe-30OCT2025 to the newly established Stablecoin E-Mode. PT-USDe represents the principal token of USDe, expiring on October 30, 2025. Like other Pendle PTs, its price is discovered through market trading but converges to 1 at maturity, reflecting its guaranteed redemption value. This pricing path is shaped by the discounting effect of implied yield and the remaining time to maturity, with the Pendle AMM concentrating liquidity closer to parity as expiry approaches. As illustrated below, the current minimum price for PT-USDe-30OCT2025 is approximately 0.975 USDe.

Supply Cap

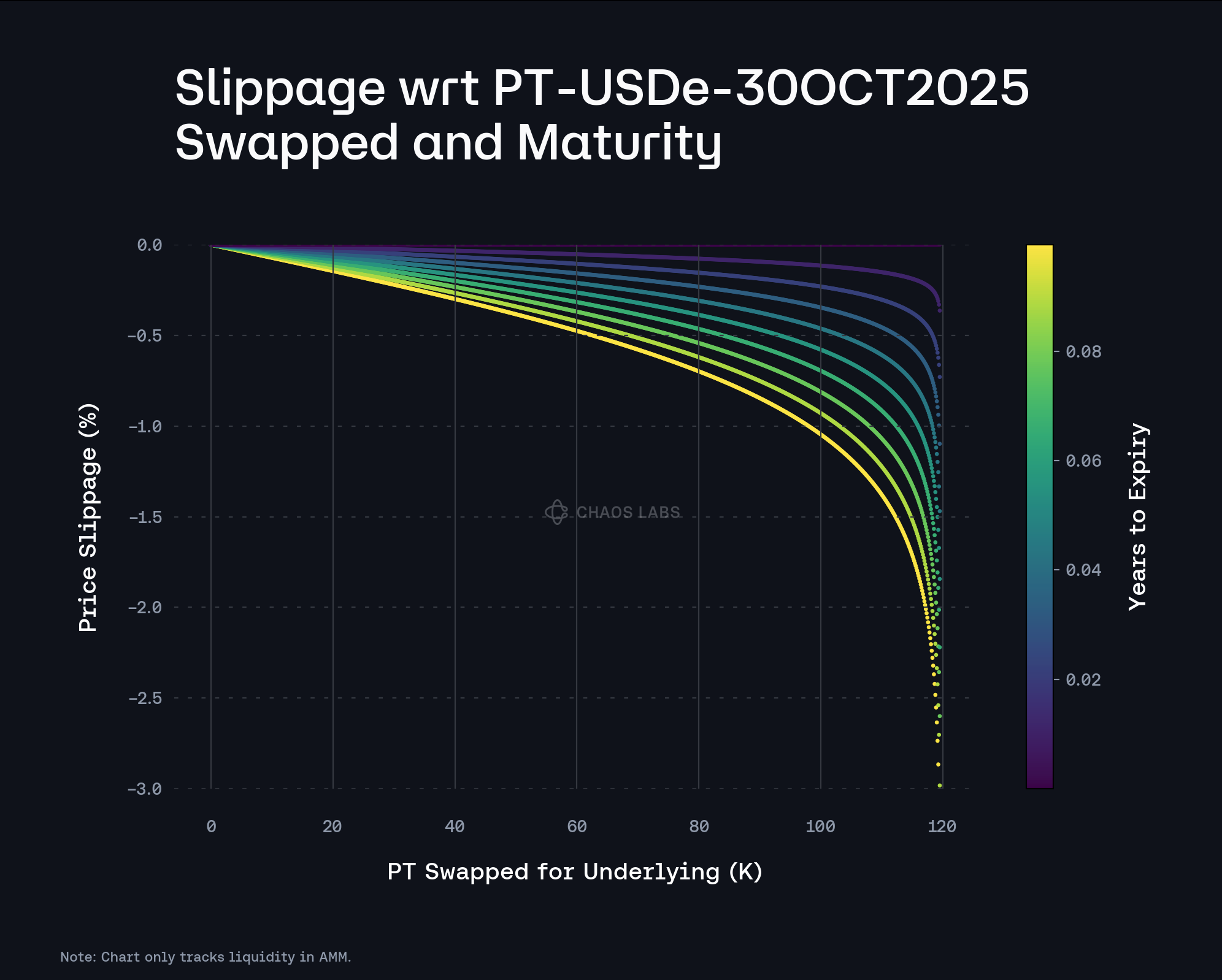

The chart below illustrates the slippage within Pendle’s native AMM when swapping PT-USDe-25OCT2025 into the underlying. At the time of writing, liquidity only supports swaps of roughly 120K before incurring 3% slippage, underscoring the limited depth of the pool. This reflects the first step of the redemption path, where PT is exchanged for SY, and SY is then unwrapped atomically into the underlying asset.

The second step under normal conditions is that the underlying asset can be traded directly into more liquid tokens. However, in the case of PT-USDe, the underlying, USDe, is not native to the BNB chain. While bridging via LayerZero’s OFT standard enables USDe transfers in just a few minutes, it still introduces additional settlement latency and operational complexity compared to native liquidity. Given these constraints, we recommend setting the supply cap conservatively at 1M.

Collateral Factor, LT, and LI

Given the expected looping use, we propose making PT-USDe-30OCT2025 non-collateralizable and non-borrowable in the core market, and only usable as collateral in the stablecoin E-Mode.

Although PT-USDe’s expected similar price trajectory with the debt asset might support more permissive parameters, conservative settings are warranted for PT-USDe-30OCT2025 due to several concerns. First, the token carries a minor to moderate level of duration risk, as yield shifts can still influence PT pricing while time remains to maturity. In addition, the underlying asset, USDe, is not native to BNB, meaning redemptions into more liquid assets may require bridging via LayerZero, which introduces settlement latency.

Furthermore, Pendle’s AMM is structurally bounded by a maximum implied yield range, and if this range is breached the PT price falls outside the AMM’s effective curve. Because liquidity in the pool is relatively shallow, even moderate-sized trades can push the pool toward its imbalance threshold, effectively forcing the AMM oracle to pin at its minimum PT price. At that point, on-chain price discovery freezes while trading may continue at lower levels on the order book. As a result, two additional risks emerge: protocols relying on the AMM oracle may overstate PT collateral value, and liquidations become more difficult as AMM liquidity dries up, leaving only fragmented order book liquidity.

Taken together, these factors highlight the importance of a slightly conservative collateral settings. Specifically, we recommend setting CF at 90%, LT at 92%, and LI at 8%.

Pricing

If we reference the previous methodology for pricing PT-USDe, our recommendation was to use a combined oracle that incorporates Pendle’s 30-minute TWAP for the PT-USDe/USDe market rate together with the Chainlink’s USDe/USD feed.

However, in this post we also propose a new pricing mechanism for USDe, as we believe it offers a more efficient approach while remaining well-contained from a risk perspective. Specifically, we recommend using Venus’s Resilient Oracle framework, configured with the USDT/USD Chainlink price feed as the main oracle, and the USDe/USD Chainlink feed as both pivot and fallback. In line with this, we suggest setting the validation bounds between the main and pivot/fallback oracles at 0.94–1.06. This design effectively insulates pricing from USDe’s short-term volatility by relying on the USDT/USD oracle under normal conditions. At the same time, we believe this configuration strikes the right balance: preventing unnecessary liquidation cascades during temporary depegs while still ensuring protection if a genuine structural failure occurs, as the 6% tolerance reflects approximately twice the largest temporary depeg observed for USDe (around 0.97) across multiple chains over the past 18 months.

If Venus adopts the resilient oracle approach for pricing USDe, based on the reasoning outlined above, we believe it would be prudent to slightly increase the risk parameters for PT-USDe, sUSDe, and USDe within the stablecoin E-Mode. Accordingly, in the specification section we provide two sets of E-Mode risk parameters, reflecting the outcomes under both pricing methodologies.

Specification

BNB Core

| Parameter | Value |

|---|---|

| Asset | PT-USDe-30OCT2025 |

| Collateral | No |

| Borrowable | No |

| Supply Cap | 1,000,000 |

| Borrow Cap | - |

| Collateral Factor | - |

| Liquidation Threshold | - |

| Liquidation Incentive | - |

| Kink | - |

| Base | - |

| Multiplier | - |

| JumpMultiplier | - |

Stablecoin E-Mode Parameters (USDe priced via USDe/USD Chainlink Oracle)

| Parameter | Value | Value | Value | Value | Value |

|---|---|---|---|---|---|

| Asset | sUSDe | USDe | PT-USDe-30OCT2025 | USDT | USDC |

| Collateral | Yes | Yes | Yes | No | No |

| Borrowable | No | Yes | No | Yes | Yes |

| Collateral Factor | 89% | 90% | 90% | - | - |

| Liquidation Threshold | 91% | 92% | 92% | - | - |

| Liquidation Incentive | 8% | 6% | 8% | - | - |

Stablecoin E-Mode Parameters (USDe priced via Resilient Oracle with USDT/USD Chainlink Oracle as core and USDe/USD Chainlink Oracle as pivot/fallback)

| Parameter | Value | Value | Value | Value | Value |

|---|---|---|---|---|---|

| Asset | sUSDe | USDe | PT-USDe-30OCT2025 | USDT | USDC |

| Collateral | Yes | Yes | Yes | No | No |

| Borrowable | No | Yes | No | Yes | Yes |

| Collateral Factor | 89.5% | 90% | 90.5% | - | - |

| Liquidation Threshold | 91.5% | 92.5% | 92.5% | - | - |

| Liquidation Incentive | 8% | 6% | 8% | - | - |

PT-USDe-30OCT2025 CAPO Parameter

| Parameter | Value |

|---|---|

| Annual Growth Rate | 0.00% |

| Snapshot Interval | 30d |

| Snapshot Gap | 4% |

Disclaimer

Chaos Labs has not been compensated by any third party for publishing this recommendation.