Summary

We recommend deprecating Venus Protocol Core deployments on opBNB, Optimism, and Unichain following sustained declines in chain-wide liquidity and usage, or limited market adoption, as well as the actively sunset Isolated Pools.

Motivation

Core markets

Venus operates core markets across eight chains. BNB Chain generates ~99% of protocol revenue:

| Market | Total Deposits | Annualized Interest Revenue (Current) | Borrows | TVL % | Revenue % |

|---|---|---|---|---|---|

| BNB Core | $1.7B | $1.8M | $485M | 99.4% | 98.9% |

| Ethereum Core | $5.3M | $8k | $1.6M | 0.3% | 0.4% |

| Arbitrum Core | $2.8M | $4k | $640K | 0.2% | 0.2% |

| zkSync Core | $2.7M | $8k | $740K | 0.2% | 0.4% |

| Unichain Core | $110K | $200 | $27K | 0.01% | <0.1% |

| Base Core | $47K | $100 | $5K | 0.00% | <0.1% |

| Optimism Core | $32K | <$100 | $4K | 0.00% | <0.1% |

| opBNB Core | $13K | <$100 | <$1k | 0.00% | <0.1% |

| Total | $1.7B | ~$1.8M | $488M |

The three targeted chains generate ~$300/year combined - less than 0.02% of protocol revenue. None has meaningful borrow activity. Base, while similarly small, is excluded from this proposal: the Base ecosystem remains healthy and Venus is actively developing a strategy to expand its presence there. Each deployment carries fixed operational costs regardless of TVL: oracle feed maintenance, guardian multisig operations, cross-chain governance bridge infrastructure, risk monitoring, and UI support.

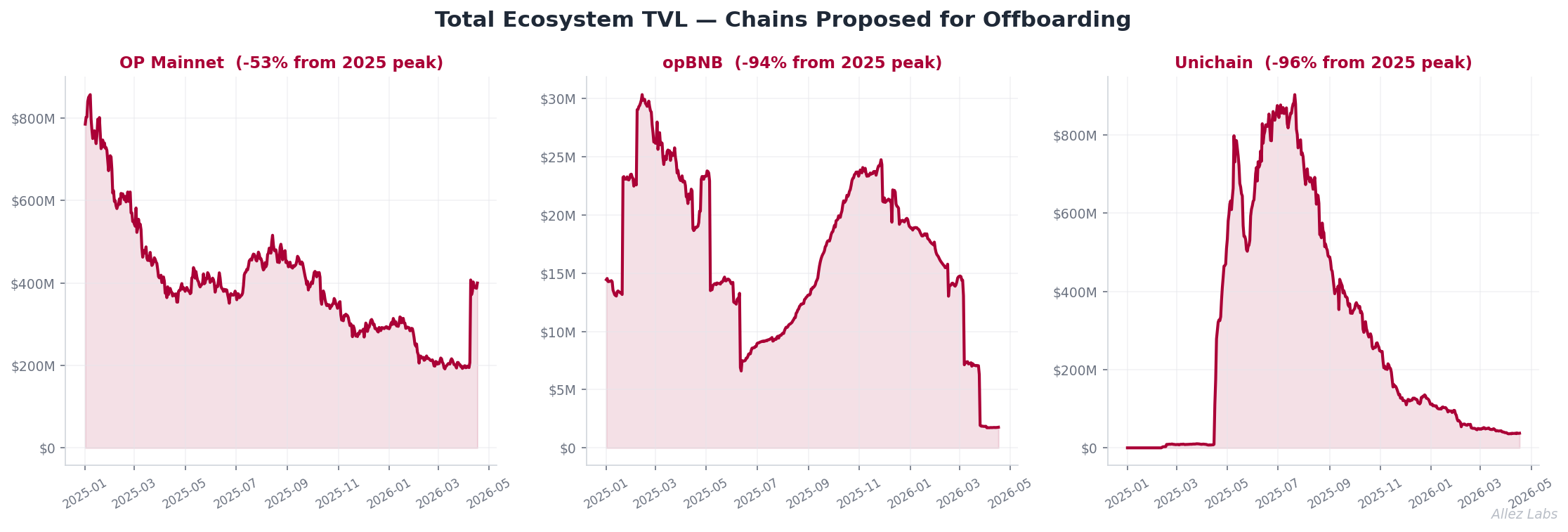

The underlying ecosystems are also contracting with the exception of Base which retains strong adoption. Total chain TVL change since the peak:

| Chain | Peak Chain TVL Since Jan 1 2025 | Current Chain TVL | Decline |

|---|---|---|---|

| Unichain | $903M | $37M | -96% |

| opBNB | $30M | $2M | -94% |

| OP Mainnet | $857M | $387M | -53% |

| Base | $5.6B | $4.6B | -18% |

Optimism’s ecosystem has held up better, but Venus never achieved meaningful traction there, currently holding $32K in total deposits.

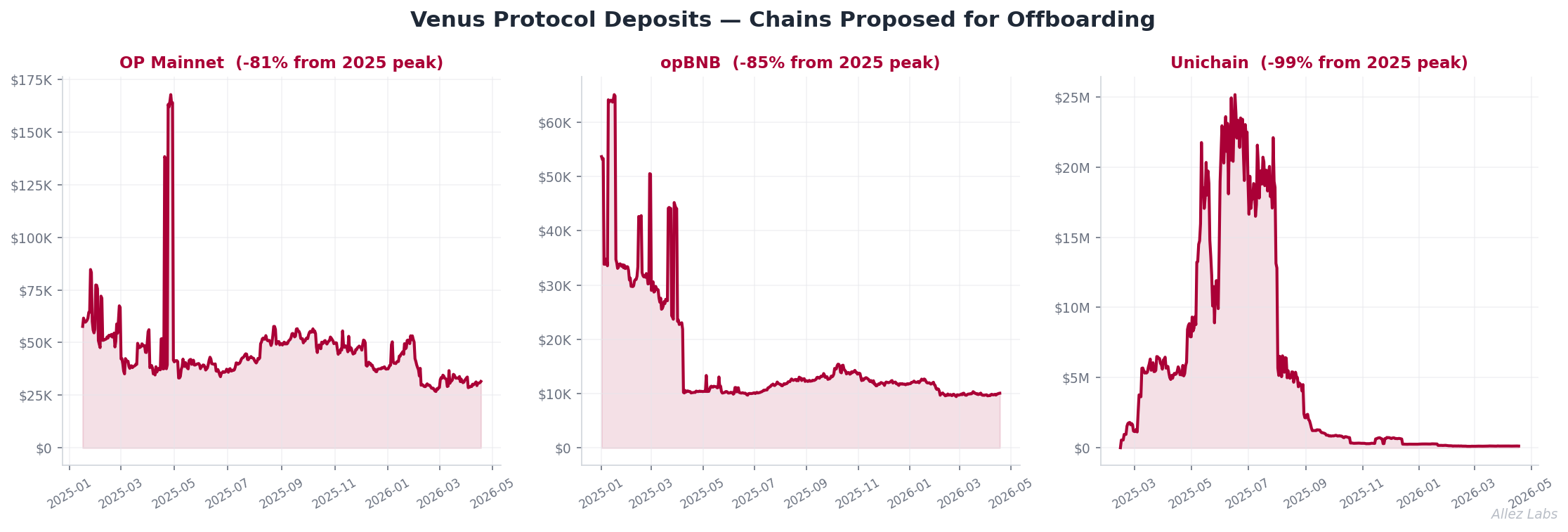

Venus protocol TVL on these chains has declined rapidly as well:

These deployments were part of a multi-chain expansion, however, the activity that would justify continued maintenance never arrived. Each chain carries operational risk, including oracle maintenance, bridge dependencies, and monitoring - while amounting to under $300/year in combined revenue and an inactive user base.

Isolated Markets

Isolated markets have been sunset since December 2025, due to their low adoption and revenue generation. Currently these markets facilitate ~$2M in deposits and <$500k in debt across the 8 isolated markets, we suggest actively deprecating these sunset pools in the same manner as the core pools outlined above.

This recommendation implements Part 3 of the sunset plan - raising reserve factors to incentivize migration. Users unwinding isolated positions are encouraged to migrate to the core pool when possible, where E-Mode groups now provide the same risk-isolation function with substantially deeper liquidity - the central rationale for the original sunset.

| Isolated Pools | Total Deposits | Total Borrow |

|---|---|---|

| BTC | $19,590 | <$0.01 |

| DeFi | $186,230 | $5,220 |

| GameFi | $894,870 | $174,270 |

| Liquid Staked BNB | $743,230 | $286,000 |

| Liquid Staked ETH | $16,040 | $371.55 |

| Meme | $25,210 | $1,520 |

| Stablecoins | $49,150 | $1,210 |

| Tron | $86,050 | $442.99 |

| Total | ~$2.02M | ~$469K |

Specification

Phase 1 - Now

Set Borrow Cap to 0; Supply Cap to 0; Collateral Factor to 0

On all assets on opBNB, Optimism, and Unichain as well as BNB isolated pools. No new borrow positions can be opened against any collateral, and no new deposits can be made to increase position borrow power. Existing positions are unaffected.

Phase 2+: Deprecation Schedule

For each of the markets, reserve factors will then be raised on the schedule below. RF increases are a soft wind-down lever because they act on both sides of the market. As RF rises, suppliers receive a smaller share of accrued interest and withdraw, which pushes utilization higher. Higher utilization drives borrow rates up along the IR curve, which in turn incentivizes borrowers to repay. Supply and borrow sides both drain without touching existing repayment terms or forcing liquidations. The stepwise ramp (→ 50% → 99%) gives users a window to act at each stage rather than collapsing yields abruptly. After Phase 3, any residual borrows will be addressed in the Phase 4 follow-up assessment.

| Phase | Timing | Action |

|---|---|---|

| Phase 1 | April 23 2026 | Borrow caps → 0, Collateral factors → 0, Supply Caps → 0 |

| Phase 2 | +2 weeks (May 6 2026) | Reserve factors → 50% on all assets |

| Phase 3 | +4 weeks (May 20 2026) | Reserve factors → 99% on all assets |

| Phase 4 | +6 weeks (June 3 2026) | Follow-up risk assessment and final wind-down steps which may include IR adjustments designed to encourage deleveraging |